What’s the Difference between Pik And Accrued Interest? A Complete Guide

The difference between PIK and accrued interest is that PIK stands for “payment-in-kind,” while accrued interest refers to the amount of interest that has been earned but not yet paid. PIK allows borrowers to make interest payments in the form of additional debt rather than cash, while accrued interest represents the amount of interest that has accumulated over a given period of time.

Interest is a common term in the world of finance, but it can be confusing to navigate the various types and methods of payment. Two terms that often come up in this realm are PIK and accrued interest. Understanding the difference between these two concepts is crucial for anyone involved in lending, borrowing, or investing.

We will explore the definitions of PIK and accrued interest, highlighting their distinctions and implications. By the end, you will have a clear understanding of these terms and their significance in financial transactions. So, let’s delve into the details and demystify PIK and accrued interest.

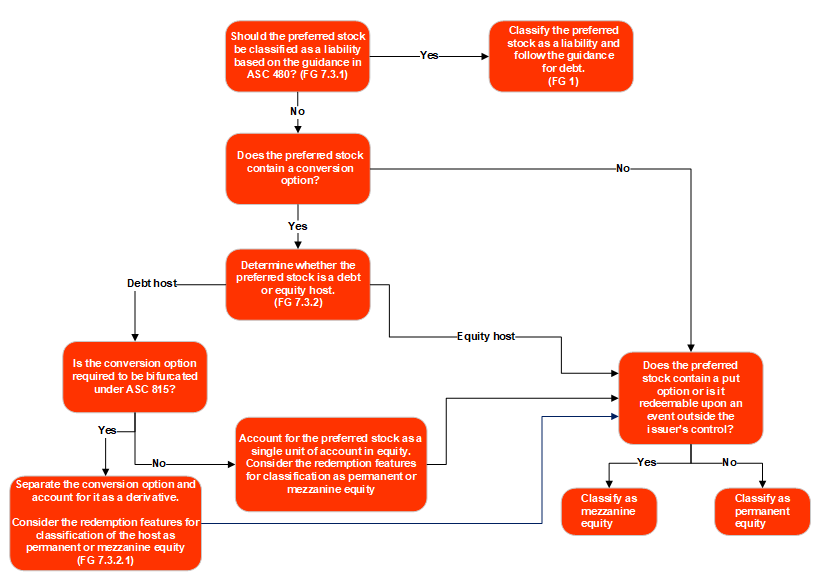

Credit: viewpoint.pwc.com

Key Differences

Pik and accrued interest are two different forms of interest payment. Pik interest refers to the payment made in kind, using additional securities or goods instead of cash. Accrued interest, on the other hand, is the interest that accumulates on a bond or loan between the interest payment dates.

Understanding the difference between pik and accrued interest is essential for anyone involved in financial transactions. While both concepts relate to interest payments, they differ significantly in their definition and calculation methods.

Definition

Pik, short for “Payment in Kind,” is a form of interest payment where the borrower has the option to pay interest using additional bonds or equity instead of cash. The lender agrees to receive these alternative forms of payment based on the terms established in the loan agreement. This allows the borrower to conserve cash flow without defaulting on interest obligations. Pik interest often carries a higher interest rate compared to cash interest.

On the other hand, accrued interest refers to the interest that has been earned but has not been paid to the lender. It accumulates over time as the borrower remains in debt or as an investment maintains its position. Accrued interest is usually calculated based on the principal amount, interest rate, and period for which the interest has been earned. It is typically paid periodically or upon the loan’s maturity.

Calculation

- Pik interest is typically calculated as a percentage of the principal amount, similar to cash interest. However, instead of being paid in cash, pik interest is paid in the form of additional securities or equity.

- Accrued interest calculation involves multiplying the principal amount, interest rate, and time period for which the interest has accrued. This calculation determines the accrued interest to be paid to the lender.

- It’s important to note that pik interest is not calculated based on time but rather on the agreement between the borrower and lender regarding the form of interest payment.

In summary, the key differences between pik and accrued interest lie in their definitions and calculation methods. While pik interest allows borrowers to pay interest using additional securities or equity, accrued interest refers to the interest that has been earned but has not been paid to the lender yet.

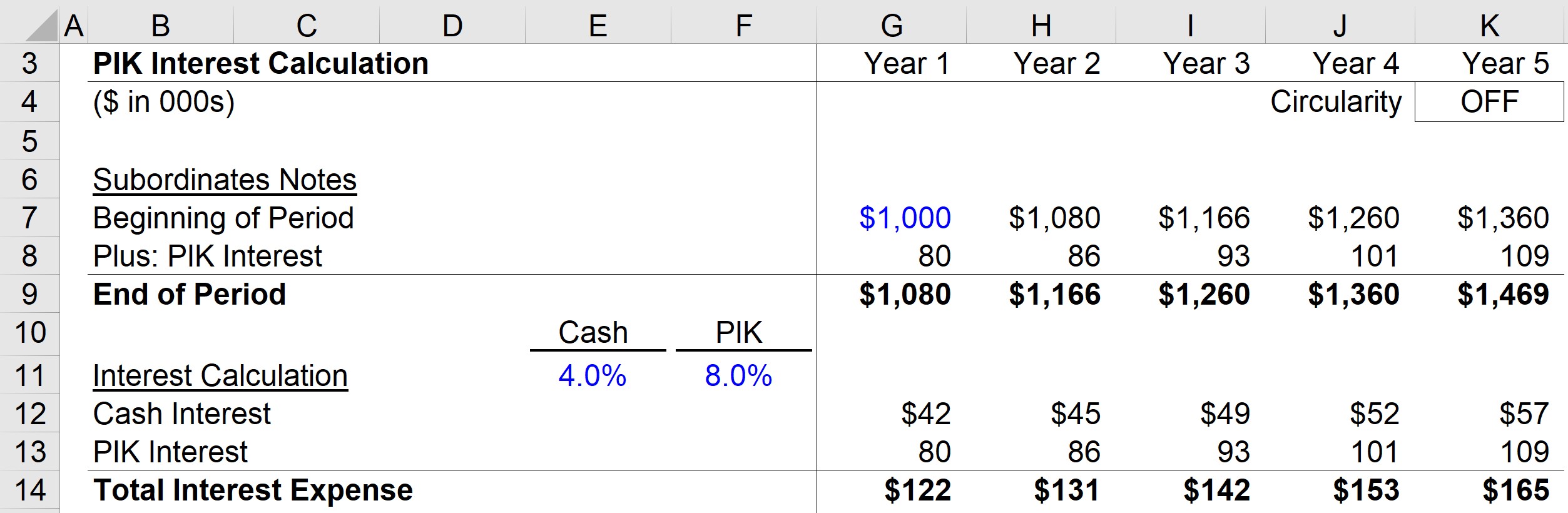

Credit: www.wallstreetprep.com

Understanding Pik Interest

PIK interest and accrued interest are two distinct financial terms. PIK interest is the form of interest where payment is made through additional securities or bonds, while accrued interest refers to the interest that has accumulated but hasn’t been paid yet.

Knowing the difference between them is important for understanding financial transactions.

Explanation

Let’s dive into the world of PIK interest and explore what it is all about. PIK stands for “payment-in-kind,” and it refers to an alternative form of interest payment. Unlike traditional interest payments that are made in cash, PIK interest allows borrowers to pay their interest using additional bonds or securities. This means that instead of receiving cash payments, lenders receive more of the borrower’s debt, which increases the principal amount owed.Usage In Finance

PIK interest finds its utilization in various financial transactions. One common use is in leveraged buyouts (LBOs), where companies acquire other companies using a significant amount of debt. In such situations, the acquiring company might prefer to pay interest on the debt in the form of additional bonds instead of cash. This allows them to conserve their cash flow and redirect it towards other operational needs or investments. Another scenario where PIK interest is employed is in distressed debt situations. When a company is facing financial difficulties and struggles to meet its cash obligations, it may negotiate with its creditors to pay interest in the form of PIK. This arrangement provides temporary relief to the company while allowing it to still fulfill its interest obligations. Furthermore, PIK interest is sometimes used as a tool to incentivize investors. In certain investment vehicles, such as convertible bonds or preferred equity, investors may be offered the option to receive interest payments in the form of additional securities. This gives them the potential to benefit from future appreciation of the borrower’s value. Overall, the utilization of PIK interest in finance provides flexibility to borrowers and allows them to manage their cash flow in unique ways. However, it is important to note that PIK interest typically carries higher risk compared to traditional interest payments, as it increases the borrower’s total debt and can lead to higher interest expenses down the line. In conclusion, understanding PIK interest is crucial in navigating the complexities of financial transactions. By comprehending its explanation and becoming familiar with its usage in finance, individuals and businesses can make informed decisions when evaluating different interest payment options.Understanding Accrued Interest

Understanding accrued interest is an essential aspect of investing that every investor should grasp. Accrued interest plays a significant role in the financial world, particularly in the bond market. This article will outline the significance of accrued interest in investing and offer a comprehensive explanation.

Explanation

Accrued interest refers to the interest that has been earned on a fixed-income investment, such as a bond, but has not been paid yet. When an investor purchases a bond between interest payment dates, they are entitled to receive the interest that has been earned from the previous interest payment date up to the settlement date. This earned but unpaid interest is known as accrued interest.

Importance In Investing

Accrued interest is crucial for investors as it reflects the actual value of a bond. When buying or selling bonds in the secondary market, the accrued interest is added to the market price to determine the total cost or proceeds. Understanding the concept of accrued interest is essential for investors to accurately assess the true cost of purchasing a bond and to ensure they receive the correct amount when selling.

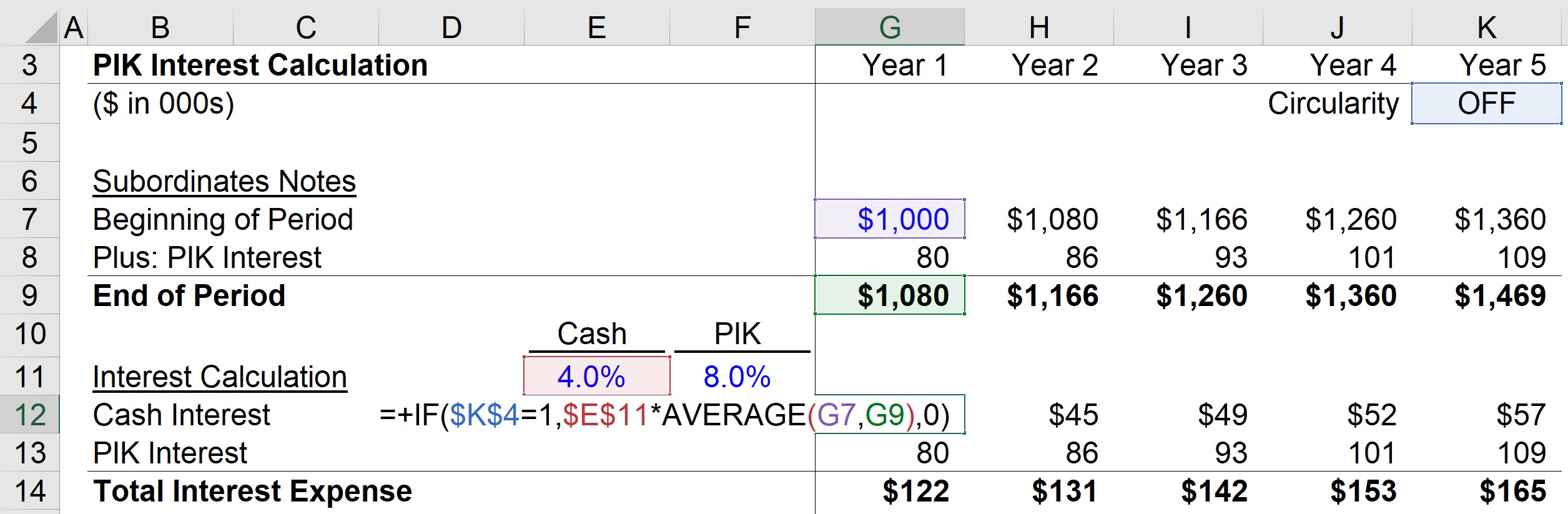

Credit: www.wallstreetprep.com

Comparison In Financial Instruments

Pik and accrued interest are two different terms in the realm of financial instruments. Pik refers to payment-in-kind, where interest is paid through additional securities instead of cash. On the other hand, accrued interest is the interest that accumulates on a bond or loan over time.

These two concepts play distinct roles in the world of finance.

Bonds

Bonds are debt instruments issued by corporations and governments to raise capital. They enable investors to lend money to the issuer in exchange for periodic interest payments and the return of the principal amount at maturity.

- Bonds represent a fixed-income investment.

- Interest payments, also known as coupon payments, are typically made semi-annually or annually.

- The bond’s face value is the amount returned to the investor at maturity.

- Risk level varies based on the issuer’s creditworthiness, with government bonds being generally considered less risky.

Loans

Loans, on the other hand, involve borrowing money from a lender with an agreement to repay the principal amount along with interest over a specified period. Loans can be obtained from banks, financial institutions, or individuals.

- Loans may have fixed or variable interest rates.

- Repayment terms can extend from months to years, depending on the loan type.

- The borrower is typically required to provide collateral or a co-signer to secure the loan.

- The loan amount is directly transferred to the borrower’s account.

Impact On Investments

Paying interest is a fundamental part of investing. The difference between PIK and accrued interest lies in how interest is paid – with PIK, it’s paid in the form of additional securities, while accrued interest is added to the principal balance.

Understanding these distinctions will help you make more informed investment decisions.

When it comes to understanding the difference between pik and accrued interest, it’s crucial to assess their impact on investments. This analysis includes evaluating the risk assessment and tax implications associated with both pik and accrued interest.Risk Assessment

Investments entail a certain level of risk, and the type of interest payment mechanism can significantly influence this factor. With pik interest, the risk may be higher compared to accrued interest. This is because pik interest allows the borrower to defer cash interest payments and instead pay them in-kind, usually by issuing additional debt. This deferral can result in increased leverage and potentially higher default risk for the issuer. On the other hand, accrued interest generally involves the regular payment of cash interest, reducing the risk of payment default. To better understand the risk assessment aspect, let’s compare pik and accrued interest using a table: Table: Risk Assessment Comparison | | Pik Interest | Accrued Interest | |———–|——————————————————–|——————————————————-| | Risk | Higher risk due to deferred cash interest payments | Lower risk with regular cash interest payments | | Leverage | Increased leverage due to the issuance of additional debt | Reduced leverage with no additional debt issuance | | Default | Higher default risk for the issuer | Lower default risk for the issuer |Tax Implications

Another essential consideration when it comes to pik and accrued interest is their tax implications. Tax implications can significantly impact the overall return on investment. In general, the tax treatment of pik interest and accrued interest may differ. However, it’s crucial to consult with a tax professional for accurate advice tailored to your specific situation. Here are some key points to understand the tax implications: – Pik interest may be treated as original issue discount (OID) for tax purposes. OID is taxed as interest income, and the tax liability arises even if there is no cash payment received. – Accrued interest is typically taxed as ordinary interest income when received. Please note that tax laws and regulations may change over time, emphasizing the importance of obtaining up-to-date information from a tax advisor. In summary, when considering the impact on investments, it is crucial to assess the risk assessment and tax implications associated with pik and accrued interest. Pik interest may introduce higher risk due to deferred cash payments and increased leverage, while accrued interest involves lower risk and regular cash payments. Additionally, understanding the tax implications ensures you are aware of any tax liabilities and can plan your investment strategies accordingly.Frequently Asked Questions Of What’s The Difference Between Pik And Accrued Interest?

What Is The Difference Between Pik And Accrued Interest?

Pik stands for payment-in-kind, a type of payment that is made in the form of additional securities or assets instead of cash. Accrued interest, on the other hand, refers to the interest that has accumulated on a financial instrument but has not been paid or received yet.

While Pik is a type of payment, accrued interest is a result of the passage of time.

How Does Pik Payment Work?

Pik payment allows borrowers to defer making cash payments on their loans by offering additional securities or assets as payment instead. This can provide more flexibility for the borrower to manage their cash flow. However, it’s important to understand the terms and conditions of the Pik arrangement, as it may have implications on the borrower’s overall financial situation.

What Is Accrued Interest Used For?

Accrued interest is used to compensate the lender or investor for the time value of money. It represents the interest that has accumulated on a financial instrument but has not yet been paid or received. Accrued interest is usually accounted for when calculating the total amount owed or to be received on a loan or investment.

Can Pik Payment Be A Good Option For Borrowers?

Pik payment can be a viable option for borrowers who are facing temporary cash flow challenges but have assets to offer as payment. It allows borrowers to manage their financial obligations while still meeting their loan requirements. However, it’s important to carefully evaluate the terms and conditions of the Pik arrangement to ensure it aligns with the borrower’s long-term financial goals.

Conclusion

Understanding the nuances between PIK and accrued interest is crucial for investors. While PIK interest is paid in the form of additional securities, accrued interest is the interest that has been earned but not yet paid. Clear comprehension of these distinctions is vital for making informed investment decisions.

Delving deeper into these concepts can empower investors to navigate the financial landscape with confidence.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is the difference between Pik and Accrued Interest?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Pik stands for payment-in-kind, a type of payment that is made in the form of additional securities or assets instead of cash. Accrued interest, on the other hand, refers to the interest that has accumulated on a financial instrument but has not been paid or received yet. While Pik is a type of payment, accrued interest is a result of the passage of time.” } } , { “@type”: “Question”, “name”: “How does Pik payment work?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Pik payment allows borrowers to defer making cash payments on their loans by offering additional securities or assets as payment instead. This can provide more flexibility for the borrower to manage their cash flow. However, it’s important to understand the terms and conditions of the Pik arrangement, as it may have implications on the borrower’s overall financial situation.” } } , { “@type”: “Question”, “name”: “What is accrued interest used for?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Accrued interest is used to compensate the lender or investor for the time value of money. It represents the interest that has accumulated on a financial instrument but has not yet been paid or received. Accrued interest is usually accounted for when calculating the total amount owed or to be received on a loan or investment.” } } , { “@type”: “Question”, “name”: “Can Pik payment be a good option for borrowers?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Pik payment can be a viable option for borrowers who are facing temporary cash flow challenges but have assets to offer as payment. It allows borrowers to manage their financial obligations while still meeting their loan requirements. However, it’s important to carefully evaluate the terms and conditions of the Pik arrangement to ensure it aligns with the borrower’s long-term financial goals.” } } ] }