What Does Amortization Mean in a Mortgage? Essential Guide!

Amortization in a mortgage refers to the process of paying off the loan over time through regular installments that include both principal and interest. With each payment, the loan balance decreases until it is fully repaid.

This commonly used method allows borrowers to budget, as they know exactly how much they need to pay each month until the mortgage is paid off. By understanding the concept of amortization, borrowers can make informed decisions about their mortgage, assess their long-term financial commitments, and calculate the total amount paid over the loan term.

Overall, amortization plays a crucial role in the structure and repayment of mortgages.

Credit: www.wallstreetprep.com

The Basics Of Amortization

Understanding the concept of amortization is crucial when it comes to mortgage payments. Amortization refers to the gradual repayment of a loan over time, typically through regular monthly installments. It involves breaking down the loan amount into smaller, manageable payments, which consist of both principal and interest. By familiarizing yourself with the basics of amortization, you can make more informed decisions about your mortgage, budgeting, and long-term financial goals.

Explanation Of Amortization

Amortization is a method used to calculate and distribute loan payments over a set period of time. When you take out a mortgage, the total amount borrowed, known as the principal, is divided into equal installments. These installments, often made monthly, include both a portion of the principal amount and the interest charged by the lender. As you make these regular payments, the outstanding loan balance gradually decreases, while the interest portion decreases over time.

Key Concepts

To better understand how amortization works, it’s important to grasp a few key concepts:

- Principal: The initial amount borrowed, which is divided into portions to be repaid over time.

- Interest: The fee charged by the lender for borrowing the principal amount. It is a percentage of the outstanding balance.

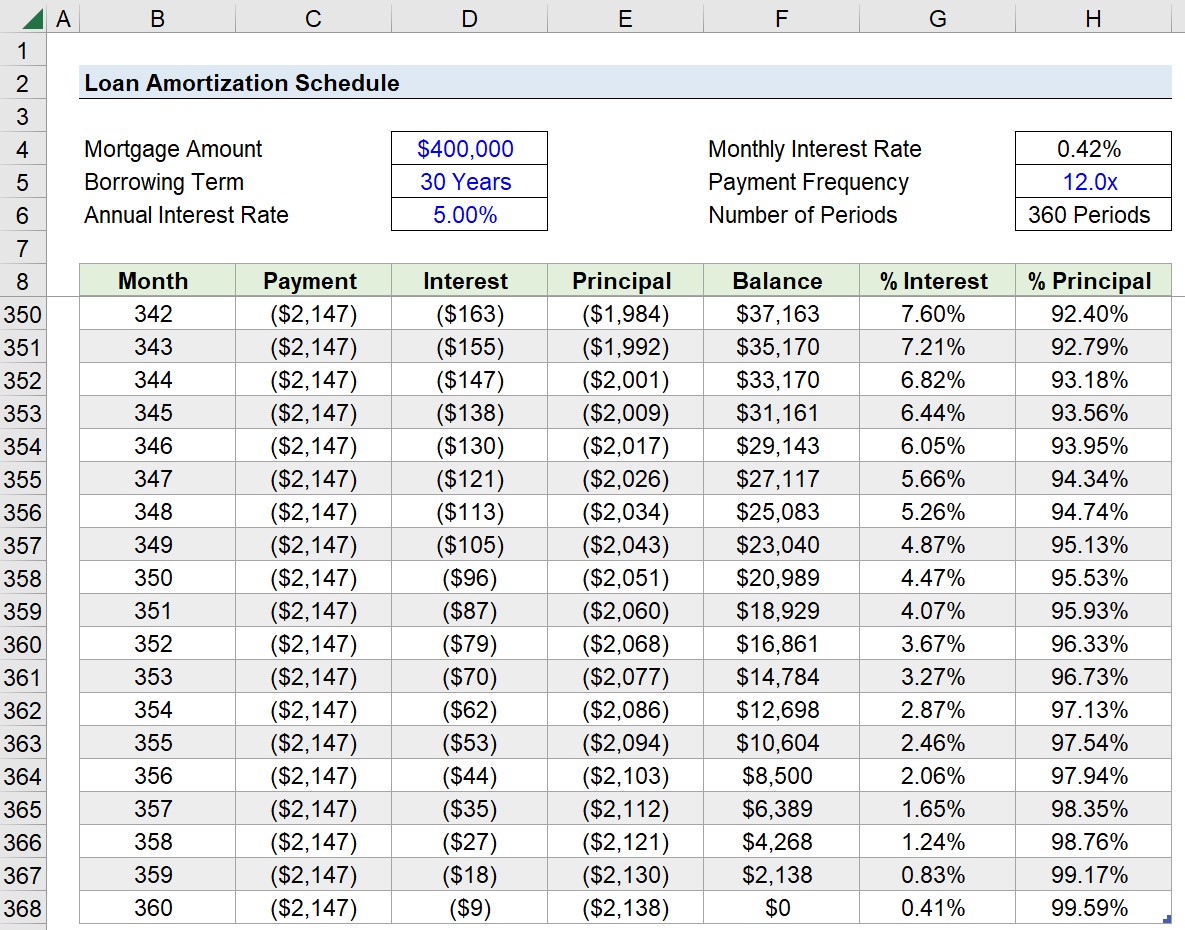

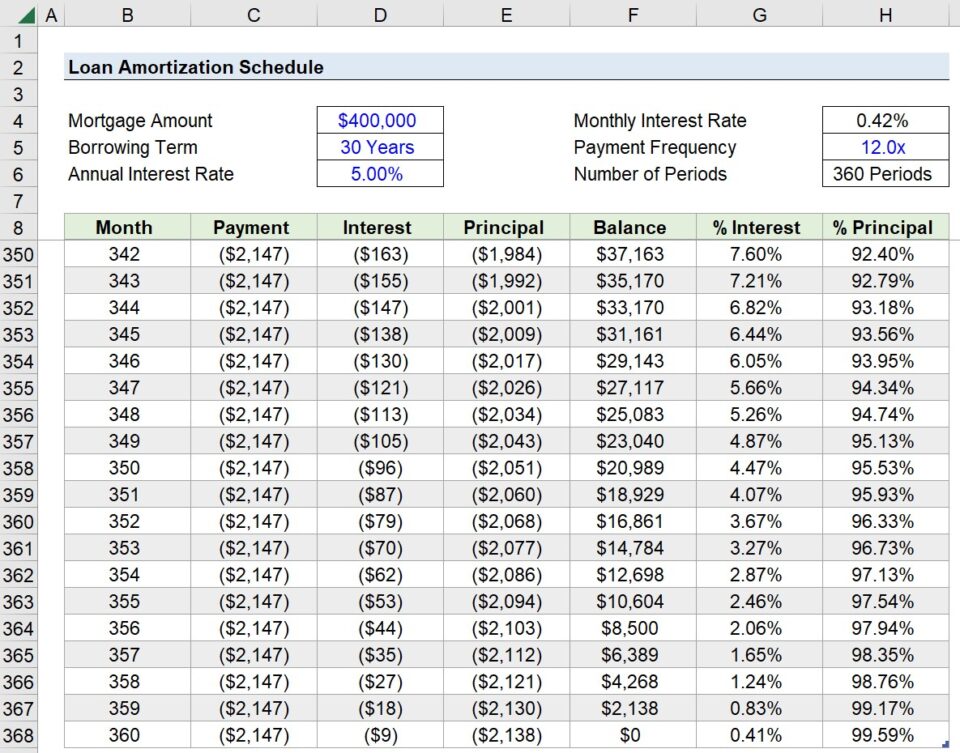

- Amortization Schedule: A table or chart that displays the breakdown of each payment made during the term of the loan, showing the principal and interest portions.

- Loan Term: The length of time agreed upon to repay the loan in full.

- Equity: The portion of the property you actually own, which increases as you pay down the principal and the property value appreciates.

Throughout the loan term, the allocation of each payment towards principal and interest changes. Initially, a larger proportion of the payment goes towards interest, while the principal portion is relatively smaller. As time goes on, this balance shifts, with a greater amount going towards reducing the principal. By the end of the loan term, both the principal and interest are fully paid off, resulting in the borrower owning the property outright.

Understanding the basics of amortization allows you to plan your finances and make informed decisions related to your mortgage. By knowing how your payments are distributed and the impact they have on the outstanding balance, you can assess your progress towards building equity and evaluate potential refinancing options. Whether you’re a first-time homebuyer or a seasoned homeowner, having a solid understanding of amortization can empower you to navigate the world of mortgages more effectively.

How Amortization Works In A Mortgage

Mortgage amortization refers to the process of paying off a mortgage loan over time through regular payments. It’s essential to understand how amortization works in a mortgage because it affects your monthly payments, the distribution of principal and interest, and the overall loan balance. Let’s dive deeper into the mechanics of amortization in a mortgage to gain a clearer understanding.

Principal And Interest Payments

When you make monthly mortgage payments, a portion of the payment goes towards paying off the loan’s principal, while the remaining amount covers the interest charged by the lender. Principal represents the actual amount you borrowed, while the interest is the cost of borrowing that money. With each payment, the proportion of principal and interest changes.

Table 1: Illustration of Principal and Interest Payments

Impact On Loan Balance Over Time

As you continue making regular mortgage payments, the loan balance gradually decreases over time. This reduction occurs due to the payment of both principal and interest. Initially, a significant portion of your payments covers interest, while a smaller portion goes towards the principal. However, as the loan balance shrinks, the proportion of principal repaid increases, and the interest charged decreases.

Understanding amortization in a mortgage empowers you to make informed financial decisions. By having a clear grasp of how your principal and interest payments are allocated and how the loan balance changes over time, you can effectively manage your mortgage and plan for the future.

Understanding Mortgage Amortization Schedules

When you obtain a mortgage to purchase a home, understanding the concept of amortization is crucial. An amortization schedule is a detailed table that illustrates how each mortgage payment is split between principal and interest over the loan term. Let’s delve into the specifics of mortgage amortization schedules and gain a deeper understanding of what it entails.

Defining Amortization Schedule

An amortization schedule is a table that outlines the breakdown of each mortgage payment into principal and interest. It displays the remaining balance of the loan after each payment, giving you a clear picture of how your mortgage will be paid off over time.

Components Of An Amortization Schedule

The components of an amortization schedule typically include the payment number, payment amount, the portion of each payment that goes towards interest, the portion that goes towards principal, and the remaining loan balance. These components provide a comprehensive overview of the entire mortgage repayment process.

Credit: www.wallstreetprep.com

Impact Of Amortization On Total Interest Paid

Amortization in a mortgage means gradual repayment of the principal amount along with interest over time. As the loan matures, the proportion of monthly payments that goes towards interest decreases, leading to a reduction in total interest paid over the loan term.

This can result in significant long-term savings for the borrower.

Understanding the concept of amortization is crucial when it comes to comprehending the true cost of a mortgage. As you make monthly payments, the principal amount gradually decreases, while the interest expenses decrease too. The impact of amortization on total interest paid is significant, with the majority of interest being paid during the early years of the mortgage term.

Interest Expenses In Early Years

During the early years of your mortgage, a substantial portion of your monthly payment goes towards paying off the interest charges. This is due to the way amortization works, where your payments initially focus on interest rather than principal. As the loan term progresses, the proportion of your payment allocated to reducing the principal increases, and the interest charges gradually decrease.

Reducing Interest Costs Through Prepayment

If you are looking to reduce the overall interest costs of your mortgage, prepayment can be an effective strategy. Making additional payments towards the principal can significantly decrease the total interest you end up paying over the life of the loan. By reducing the principal balance earlier, you are essentially shortening the loan term and reducing the time for interest to accrue.

However, it is essential to carefully consider the terms of your mortgage before making prepayments. Some loans may have prepayment penalties or specific rules regarding additional payments. Take the time to review your mortgage agreement and consult with a financial advisor to determine the best approach for your specific situation.

In conclusion, understanding how amortization works is crucial to fully grasp the impact it has on the total interest paid over the life of a mortgage. The majority of interest expenses are incurred during the early years, while prepayment can be a valuable strategy for reducing overall interest costs. By making informed decisions about your mortgage, you can save money and potentially pay off your loan sooner.

Comparing Different Amortization Methods

When you take out a mortgage, understanding how your loan will be repaid is essential. Amortization refers to the process by which you gradually pay off your mortgage over time through regular installments. While the concept of amortization itself is fairly straightforward, there are different methods to consider when it comes to repaying your loan.

Fixed-rate Vs. Adjustable-rate Mortgages

One of the key factors that determine your mortgage amortization is the type of mortgage you choose. Fixed-rate and adjustable-rate mortgages are the two primary options available to borrowers.

Fixed-rate mortgages offer stability and predictability as the interest rate remains the same throughout the loan term. This means your monthly payments will always be the same, making it easier to budget for the long term.

Adjustable-rate mortgages (ARMs), on the other hand, have interest rates that can fluctuate over time. Initially, an ARM may start with a lower interest rate compared to a fixed-rate mortgage. However, the rate can vary periodically, frequently resulting in changes to your monthly payment amount.

Implications For Borrowers

Each amortization method has its unique factors to consider, which can directly impact borrowers in various ways.

With a fixed-rate mortgage, you can enjoy the peace of mind that comes from knowing your monthly payment will remain constant. This stability is particularly beneficial in times of economic uncertainty or rising interest rates, as it shields you from potential payment shocks. Additionally, a fixed-rate mortgage allows you to build equity steadily over time, as a portion of each payment is applied towards the principal balance.

Borrowers who opt for an adjustable-rate mortgage may benefit if interest rates are expected to decrease in the future. The initial lower interest rate could provide some short-term savings on your monthly payment. However, it is important to carefully consider the impact of potential rate increases down the line, as this could significantly impact your budget. With an ARM, you may also have the opportunity to refinance your loan or sell your property before the rate adjustments occur.

When comparing different amortization methods, it’s crucial to assess your financial situation, preferences, and long-term goals. By understanding the implications of fixed-rate and adjustable-rate mortgages, you can make an informed decision about which option aligns best with your needs and financial capabilities.

Credit: bluewatermtg.com

Frequently Asked Questions Of What Does Amortization Mean In A Mortgage?

What Is The Meaning Of Amortization In A Mortgage?

Amortization in a mortgage refers to the process of paying off your loan over time through regular payments. Payments are divided into principal (the loan amount) and interest (the cost of borrowing). Initially, more of the payment goes towards interest, but over time, it shifts towards paying down the principal.

How Does Amortization Affect Mortgage Payments?

Amortization affects mortgage payments by determining the amount you pay in each installment. As you make monthly payments, the interest portion decreases, while the principal portion increases. This leads to a gradual reduction in the outstanding loan balance, ultimately shortening the time it takes to fully repay the mortgage.

Why Is Amortization Important In A Mortgage?

Amortization is important in a mortgage because it allows borrowers to manage the repayment of their loan over time. It helps to determine the monthly payment amount and ensures that the loan is gradually paid off. By understanding the amortization process, homeowners can plan their finances and make informed decisions about their mortgage.

Conclusion

Understanding amortization is crucial for navigating the complexities of a mortgage. By spreading out loan payments, borrowers can manage their finances better. As you consider your options, keep in mind the impact of amortization on your long-term financial goals. Making informed decisions about your mortgage can lead to greater financial stability in the future.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is the meaning of amortization in a mortgage?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Amortization in a mortgage refers to the process of paying off your loan over time through regular payments. Payments are divided into principal (the loan amount) and interest (the cost of borrowing). Initially, more of the payment goes towards interest, but over time, it shifts towards paying down the principal.” } } , { “@type”: “Question”, “name”: “How does amortization affect mortgage payments?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Amortization affects mortgage payments by determining the amount you pay in each installment. As you make monthly payments, the interest portion decreases, while the principal portion increases. This leads to a gradual reduction in the outstanding loan balance, ultimately shortening the time it takes to fully repay the mortgage.” } } , { “@type”: “Question”, “name”: “Why is amortization important in a mortgage?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Amortization is important in a mortgage because it allows borrowers to manage the repayment of their loan over time. It helps to determine the monthly payment amount and ensures that the loan is gradually paid off. By understanding the amortization process, homeowners can plan their finances and make informed decisions about their mortgage.” } } ] }