What Does a 15 Year Amortization Mean? A Guide to Financial Freedom

A 15-year amortization means that the loan will be paid off in 15 years. This fixed-term mortgage option allows borrowers to pay off their loan sooner, resulting in higher monthly payments but less interest paid over time.

Introducing a 15-year amortization, commonly referred to as a 15-year fixed-rate mortgage, means committing to repaying your loan in full over a span of 15 years. Unlike longer mortgage options, like a 30-year term, this shorter duration requires borrowers to make higher monthly payments.

However, the advantage lies in the overall reduced interest paid over time. By opting for a 15-year amortization, homeowners can build equity faster and become debt-free sooner. We will explore the features and benefits of a 15-year amortization, helping you determine if this mortgage option aligns with your financial goals and circumstances.

Credit: www.wallstreetprep.com

Understanding 15 Year Amortization

When it comes to understanding mortgage terms, one of the key concepts to grasp is amortization. Amortization is the process of paying off a loan over time through regular payments that include both principal and interest. A shorter amortization period means higher monthly payments, but it also means less interest paid overall. In this article, we will focus on the importance of a 15-year amortization and how it can impact your mortgage.

What Is Amortization?

Amortization is the gradual repayment of a loan through regular payments, typically monthly. These payments are structured in a way that the loan is fully paid off by the end of the amortization period. With each payment, a portion goes towards reducing the principal balance, while the rest covers the interest accrued on the outstanding balance.

Importance Of 15 Year Amortization

A 15-year amortization period is a relatively short term for paying off a mortgage compared to other options, such as 20 or 30 years. While it may result in higher monthly payments, there are several significant advantages to choosing a 15-year amortization:

- Building Equity Faster: By opting for a 15-year amortization, you can build equity in your home faster. Since the principal balance is paid down more quickly, you accumulate home equity at a higher rate. This can be advantageous if you plan on selling your home or using the equity for future investments.

- Save Money on Interest: A shorter amortization period means less time for interest to accrue. As a result, you end up paying significantly less in interest over the life of the loan. This can amount to substantial savings, potentially tens of thousands of dollars, depending on the loan amount and interest rate.

- Faster Debt-Free Ownership: Opting for a 15-year amortization means you will be mortgage-free in half the time compared to a longer-term loan. This can provide a sense of financial freedom and security, allowing you to allocate your resources towards other financial goals or invest in other areas.

In summary, choosing a 15-year amortization for your mortgage can have numerous benefits, including faster equity building, saving money on interest, and achieving debt-free homeownership in a shorter timeframe. While the higher monthly payments may initially seem daunting, the long-term advantages cannot be overlooked. Consider discussing your options with a mortgage professional to determine if a 15-year amortization is the right choice for your financial situation.

Benefits Of 15 Year Amortization

A 15-year amortization refers to the process of paying off a loan or mortgage over a period of 15 years through regular monthly payments. This shorter timeline can offer several benefits to borrowers, including:

Accelerated Equity Build-up

With a 15-year amortization, homeowners can build equity in their property at a faster rate. This is because a larger portion of each monthly payment goes toward reducing the principal balance rather than paying interest. As the loan balance decreases more quickly, homeowners can gain more equity in their property and potentially have a higher net worth in a shorter period of time.

Lower Total Interest Costs

One of the greatest advantages of a 15-year amortization is the reduced overall interest costs. Since the loan term is shorter, the total amount of interest paid over the life of the loan is significantly lower compared to a longer-term loan. This can result in substantial savings and enable borrowers to put more money towards other financial goals, such as saving for retirement or investing in other assets.

Considerations Before Choosing 15 Year Amortization

Considering a 15-year amortization for your mortgage is a significant financial decision that requires careful thought and consideration. It’s important to assess your financial situation and future goals before choosing this option. Here are some key factors to consider before committing to a 15-year amortization:

Monthly Payment Affordability

Assess whether the higher monthly payments associated with a 15-year amortization are within your budget. Use a mortgage calculator to determine the monthly payments and ensure they align with your financial capability.

Financial Goals Assessment

Evaluate your long-term financial goals and determine if a 15-year amortization supports these objectives. Consider whether you can comfortably manage the higher payments while still meeting other financial obligations and goals, such as saving for retirement or investing.

Tips For Managing A 15 Year Amortization

Managing a 15 year amortization can be a challenging task, but with the right tips, you can stay on track and make the most of your mortgage payments. In this section, we will discuss three key tips to help you manage a 15 year amortization effectively: creating a realistic budget, exploring refinancing options, and staying proactive.

Creating A Realistic Budget

One of the first steps in managing a 15 year amortization is to create a realistic budget. Start by assessing your monthly income and expenses. Be sure to account for your mortgage payment as well as other financial obligations such as utilities, groceries, and transportation costs. This will give you a clear picture of how much you have left each month to allocate towards your mortgage.

Next, consider making adjustments to your spending habits to ensure your budget aligns with your mortgage goals. Look for opportunities to cut back on non-essential expenses and redirect those funds towards your mortgage payments. You can also explore ways to increase your income, such as taking on a side job or freelance work, to further support your mortgage repayment efforts.

By creating a realistic budget, you will have a solid foundation for managing your 15 year amortization and staying on top of your financial commitments.

Exploring Refinancing Options

If you find yourself struggling to manage your mortgage payments on a 15 year amortization, exploring refinancing options can be a beneficial strategy. Refinancing allows you to replace your current mortgage with a new one, often with different terms and a potentially lower interest rate.

Refinancing can provide several advantages, such as reducing your monthly mortgage payments, allowing you to free up extra funds for other expenses or savings. It can also help you secure a lower interest rate, which can save you thousands of dollars over the life of your loan.

However, before refinancing, it is important to carefully evaluate the associated costs and fees. Consider factors such as closing costs, prepayment penalties, and the length of time it will take to recoup any upfront expenses. By weighing these factors and comparing different refinancing options, you can make an informed decision that suits your financial situation.

Staying Proactive

Finally, staying proactive is key to effectively managing a 15 year amortization. Regularly reviewing your mortgage statements, checking for any errors or discrepancies, and monitoring your progress towards paying off your loan can help you stay on track and identify any potential issues early on.

Additionally, staying proactive also means staying informed about changes in your financial situation or mortgage terms. Stay up-to-date with current interest rates and consider taking advantage of opportunities to make extra principal payments if they align with your goals. This can help you reduce the total interest paid over the life of the loan and shorten the overall term of your mortgage.

Remember, managing a 15 year amortization requires discipline and commitment, but with these tips and a proactive mindset, you can successfully navigate through the repayment process.

Achieving Financial Freedom With 15 Year Amortization

A 15-year amortization means spreading out principal and interest payments over 15 years, leading to higher monthly payments but lower overall interest costs. It enables quicker equity growth and financial freedom compared to the traditional 30-year mortgage, making it a favorable option for long-term financial sustainability.

Achieving Financial Freedom with 15 Year Amortization Building Long-Term Wealth One of the key benefits of a 15-year amortization is the potential to build long-term wealth. With this shorter repayment period, you can pay off your mortgage faster and reduce the amount of interest you pay over time. By consistently making payments on your 15-year mortgage, you are not only building equity in your home but also increasing your net worth. This can provide you with financial stability and a solid foundation for the future. Retirement Planning Thinking about retirement can be overwhelming, but a 15-year amortization can play a crucial role in your retirement planning strategy. By opting for a shorter mortgage term, you will be mortgage-free when you retire, freeing up a significant portion of your income for other purposes. Instead of worrying about monthly mortgage payments during your retirement years, you can focus on enjoying your hard-earned savings and living the lifestyle you desire. Moreover, paying off your mortgage early can also allow you to redirect funds towards retirement savings accounts such as IRAs and 401(k)s. By investing in these accounts consistently, you can take advantage of compounding interest and maximize the growth of your retirement nest egg. When it comes to achieving financial freedom, a 15-year amortization can be a powerful tool. By building long-term wealth and ensuring a debt-free retirement, you can set yourself up for a more secure and fulfilling financial future. Take the first step towards financial independence by exploring the option of a 15-year amortization today. “`htmlBuilding Long-term Wealth

One of the key benefits of a 15-year amortization is the potential to build long-term wealth. With this shorter repayment period, you can pay off your mortgage faster and reduce the amount of interest you pay over time. By consistently making payments on your 15-year mortgage, you are not only building equity in your home but also increasing your net worth. This can provide you with financial stability and a solid foundation for the future.

Retirement Planning

Thinking about retirement can be overwhelming, but a 15-year amortization can play a crucial role in your retirement planning strategy. By opting for a shorter mortgage term, you will be mortgage-free when you retire, freeing up a significant portion of your income for other purposes. Instead of worrying about monthly mortgage payments during your retirement years, you can focus on enjoying your hard-earned savings and living the lifestyle you desire.

Moreover, paying off your mortgage early can also allow you to redirect funds towards retirement savings accounts such as IRAs and 401(k)s. By investing in these accounts consistently, you can take advantage of compounding interest and maximize the growth of your retirement nest egg.

When it comes to achieving financial freedom, a 15-year amortization can be a powerful tool. By building long-term wealth and ensuring a debt-free retirement, you can set yourself up for a more secure and fulfilling financial future. Take the first step towards financial independence by exploring the option of a 15-year amortization today.

Credit: www.wallstreetprep.com

Credit: www.bankrate.com

Frequently Asked Questions For What Does A 15 Year Amortization Mean?

What Is A 15 Year Amortization?

A 15 year amortization refers to the repayment period for a loan in which the borrower makes regular payments over 15 years, gradually reducing the principal and interest owed. This shorter term can lead to higher monthly payments, but it can also help borrowers pay off their loan faster and potentially save on interest costs.

How Does A 15 Year Amortization Differ From A 30 Year Amortization?

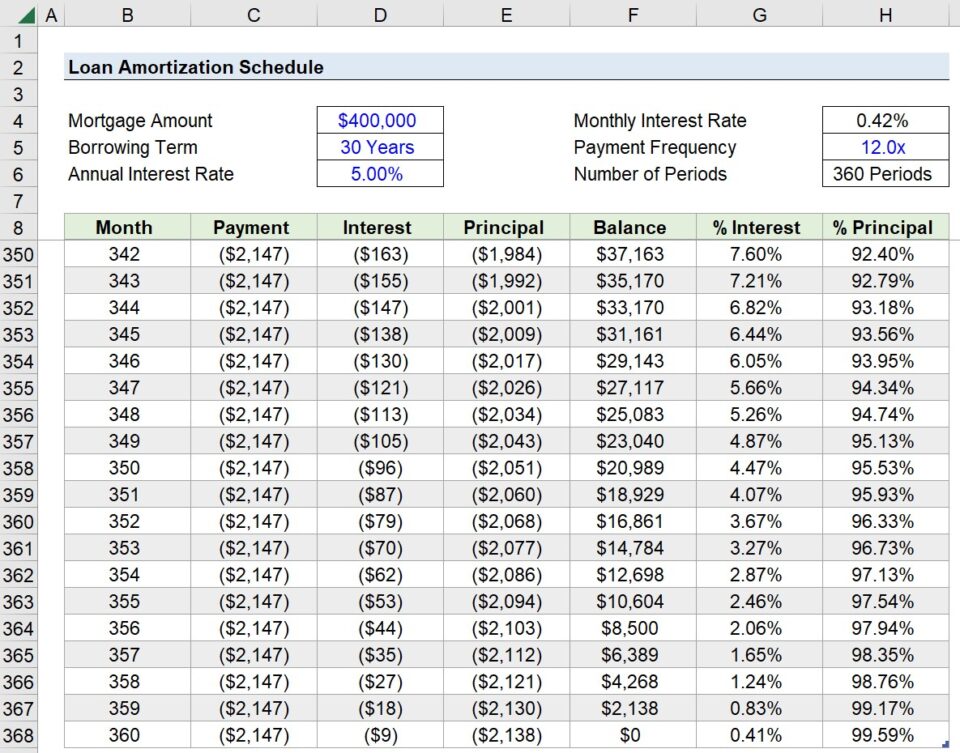

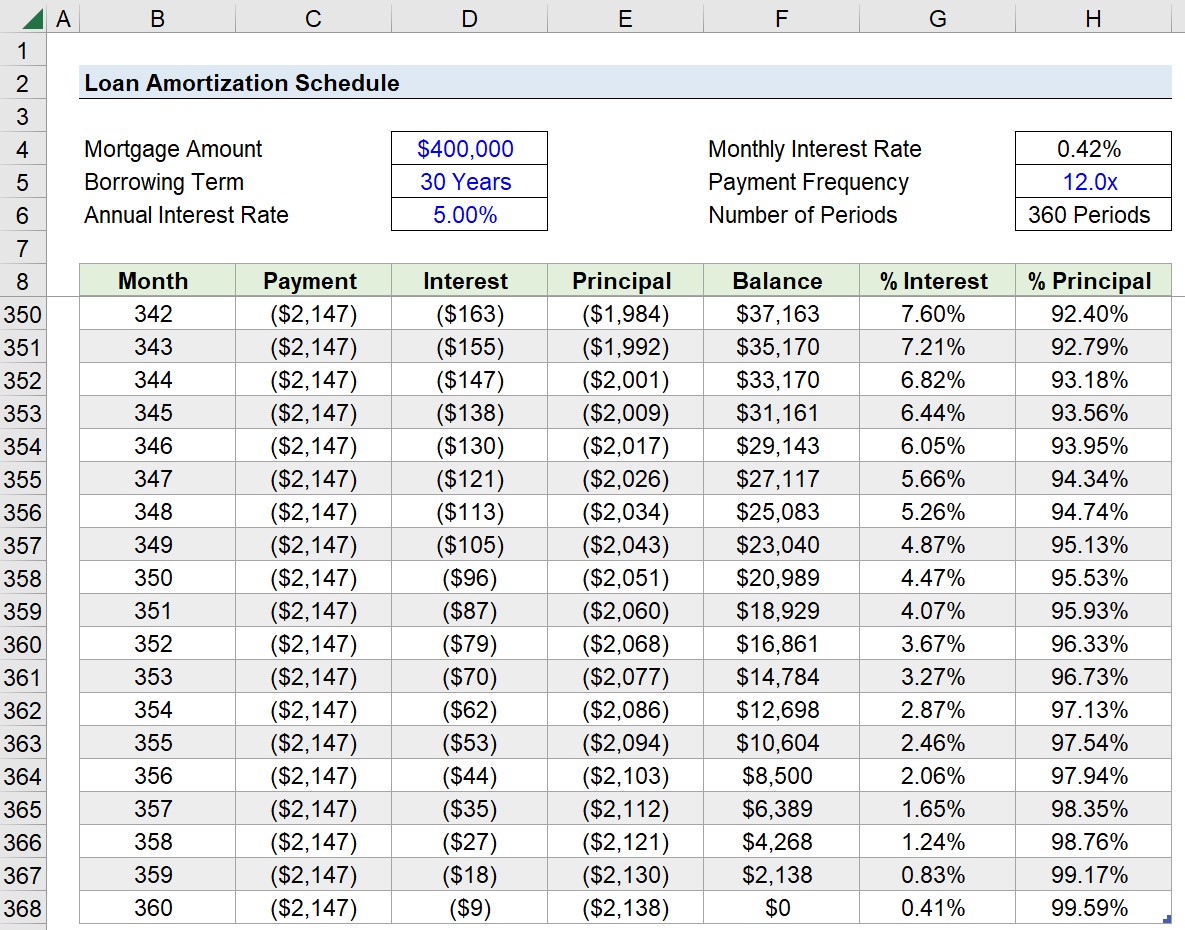

The main difference between a 15 year and 30 year amortization is the length of time it takes to pay off the loan. With a 15 year amortization, the loan is paid off in half the time compared to a 30 year amortization.

This results in higher monthly payments, but lower total interest paid over the life of the loan.

Are There Any Benefits To A 15 Year Amortization?

Yes, there are several benefits to choosing a 15 year amortization. Firstly, borrowers can build home equity more quickly due to the shorter repayment period. Additionally, the interest paid over the life of the loan is significantly less compared to a longer term loan, saving borrowers money in the long run.

However, it’s important to consider if the higher monthly payments fit within your budget.

Is A 15 Year Amortization Right For Everyone?

A 15 year amortization may not be the right choice for everyone. It is suitable for individuals who can comfortably afford higher monthly payments and who want to repay their loan quickly. However, those with limited cash flow or uncertain income may find it challenging to meet the higher monthly payments.

It’s essential to evaluate your financial situation before deciding on a 15 year amortization.

Conclusion

So, understanding a 15-year amortization is vital for any homeowner. It helps calculate total interest paid and how long it takes to pay off. Therefore, evaluating your financial situation and goals is crucial before choosing a mortgage term. Ultimately, being informed about amortization can save you money in the long run.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is a 15 Year Amortization?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “A 15 year amortization refers to the repayment period for a loan in which the borrower makes regular payments over 15 years, gradually reducing the principal and interest owed. This shorter term can lead to higher monthly payments, but it can also help borrowers pay off their loan faster and potentially save on interest costs.” } } , { “@type”: “Question”, “name”: “How does a 15 Year Amortization differ from a 30 Year Amortization?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The main difference between a 15 year and 30 year amortization is the length of time it takes to pay off the loan. With a 15 year amortization, the loan is paid off in half the time compared to a 30 year amortization. This results in higher monthly payments, but lower total interest paid over the life of the loan.” } } , { “@type”: “Question”, “name”: “Are there any benefits to a 15 Year Amortization?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, there are several benefits to choosing a 15 year amortization. Firstly, borrowers can build home equity more quickly due to the shorter repayment period. Additionally, the interest paid over the life of the loan is significantly less compared to a longer term loan, saving borrowers money in the long run. However, it’s important to consider if the higher monthly payments fit within your budget.” } } , { “@type”: “Question”, “name”: “Is a 15 Year Amortization right for everyone?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “A 15 year amortization may not be the right choice for everyone. It is suitable for individuals who can comfortably afford higher monthly payments and who want to repay their loan quickly. However, those with limited cash flow or uncertain income may find it challenging to meet the higher monthly payments. It’s essential to evaluate your financial situation before deciding on a 15 year amortization.” } } ] }