What Does 5 Year Term 20 Year Amortization Mean?: Simplified Mortgage Explained

A 5 year term with a 20 year amortization means that the loan will be repaid over a period of 20 years, but the interest rate and payment terms are fixed for the first 5 years. This allows the borrower to make smaller monthly payments during the initial 5 year period before transitioning to larger payments for the remaining 15 years.

Are you planning to take out a loan? Understanding the terms associated with loan repayment is crucial for making informed financial decisions. One such term, “5 year term with a 20 year amortization,” may seem complicated at first glance, but it can actually provide you with some flexibility.

We will break down what this term means, how it works, and what it could mean for your financial situation. So, let’s dive in and explore the concept of a 5 year term with a 20 year amortization in more detail.

:max_bytes(150000):strip_icc()/how-amortization-works-315522_FINAL-8e058e582a744f349593e5c560b46783.png)

Credit: www.thebalancemoney.com

The Basics Of Mortgage

Definition Of Mortgage

A mortgage is a loan provided by a financial institution such as a bank, that allows individuals or businesses to purchase a property. It is a legal agreement in which the borrower pledges a property as collateral to secure the loan.

Components Of A Mortgage

When you take out a mortgage, there are several components that you should be aware of:

- Principal: The principal is the original amount of money borrowed from the lender. This is the amount you will have to repay over time.

- Interest: Interest is the cost of borrowing money. It is a percentage of the principal that you will have to pay to the lender in addition to the principal amount.

- Term: The term refers to the length of time you have agreed to repay the mortgage. It is usually expressed in years, such as a 5-year term.

- Amortization: Amortization is the process of repaying the mortgage over time through regular payments. It is typically expressed in years, such as a 20-year amortization.

Now, let’s take a closer look at the relationship between the term and amortization in a mortgage.

| Term | Amortization |

|---|---|

| 5 years | 20 years |

When a mortgage has a 5-year term and a 20-year amortization, it means that the borrower has agreed to repay the loan over a period of 20 years, but the interest rate is valid for only the first 5 years. At the end of the 5-year term, the borrower would have to renegotiate the mortgage or seek a new lender.

This arrangement allows borrowers to benefit from a lower interest rate for the first 5 years, with the flexibility to reassess their financial situation and potentially take advantage of lower interest rates in the future.

Understanding the basics of a mortgage, including the components like principal, interest, term, and amortization, can help you make informed decisions when it comes to financing a property purchase. It is important to carefully consider your options and seek professional advice to ensure you choose the right mortgage for your needs.

Understanding The Terminology

When it comes to mortgages and loans, understanding the terminology is essential. Two key terms you’ll often come across are “5 Year Term” and “20 Year Amortization”. These terms represent two different aspects of a mortgage and can affect your loan repayment strategy and financial planning. In this section, we will explain what each term means and how they are relevant to your mortgage.

Explaining 5 Year Term

A 5 Year Term refers to the length of time a mortgage agreement is in effect before it needs to be renegotiated or renewed. It sets the duration during which the interest rate and other terms of your mortgage remain fixed. After the 5-year term is over, you have the option to renew your mortgage agreement, negotiate new terms, or even switch to a different lender if you choose.

During the 5-year term, you will typically make regular monthly payments towards both the principal amount borrowed and the interest accrued. The amount of your payments will be determined based on the interest rate and the amortization period.

Breaking Down 20 Year Amortization

20 Year Amortization refers to the length of time it will take to fully repay your mortgage, including both the principal and interest. It represents the number of years it will take to pay off the loan if you make regular, equal monthly payments. The longer the amortization period, the lower your monthly payments will be, but the more interest you will end up paying over time.

For example, if you have a mortgage with a 20-year amortization period, you will need to make monthly payments for 20 years to fully repay the loan. Each payment will consist of both principal and interest, gradually reducing your loan balance over time. With an amortization period of 20 years, you will have the goal of becoming mortgage-free at the end of this time frame.

Amortization periods can range from as short as 10 years to as long as 30 years, depending on your financial situation, goals, and interest rates. It is important to carefully consider the amortization period when selecting a mortgage, as it can impact the total cost of your loan and how long it will take to become debt-free.

Your Loan Repayment Strategy

Understanding the terms “5 Year Term” and “20 Year Amortization” is crucial for developing a solid loan repayment strategy. By knowing when your mortgage agreement will need to be renewed and how long it will take to fully repay your loan, you can make informed decisions about your finances and plan for the future.

When choosing a mortgage, consider your long-term financial goals, such as how quickly you want to pay off your loan and the impact of interest rates on your monthly payments. Take the time to understand the terms and conditions of your mortgage agreement, and consult with a financial professional if necessary, to ensure you make the most suitable choice for your unique circumstances.

Impact On Monthly Payments

A five-year term with a 20-year amortization means that the loan is to be paid off in five years, based on a 20-year payment schedule. This would lead to a higher monthly payment compared to that of a 30-year amortization.

The shorter term accelerates the payoff, reducing the total interest paid over the life of the loan.

Impact on Monthly Payments When it comes to understanding the impact of a 5-year term and a 20-year amortization on monthly payments, it’s crucial to dive into the specifics. The term, representing the length of the mortgage agreement, and the amortization, indicating the period to pay off the loan, both play pivotal roles in determining monthly payments. Monthly Payments with 5 Year Term The 5-year term denotes the duration for which the interest rate and mortgage conditions are set. With a shorter term, monthly payments are often higher, as the loan must be repaid over a compressed timeframe. The advantage lies in the potential interest savings and quicker equity building. Monthly Payments with 20 Year Amortization Having a 20-year amortization allows for stretching out the repayment period, thus reducing the monthly payment amount. However, the longer amortization lengthens the time it takes to pay off the loan and accumulates more interest over the life of the mortgage. By structuring these headers into your blog post, readers will gain a clear understanding of how a 5-year term and a 20-year amortization affect monthly payments when obtaining a mortgage.

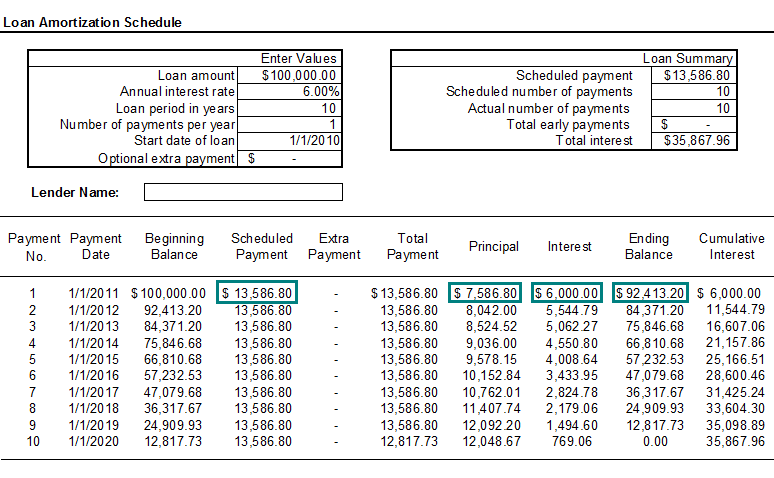

Credit: www.boe.ca.gov

Long Term Financial Implications

A 5 year term with a 20 year amortization refers to a loan agreement where the borrower makes payments based on a 20-year schedule, but the loan is expected to be fully paid off within 5 years. This can have long term financial implications as it allows for lower monthly payments, but may result in higher overall interest costs.

Understanding the long-term financial implications of a mortgage term is crucial when making a major investment, such as buying a home. One important consideration is the 5-year term with a 20-year amortization. This financing option affects both the total interest paid over 20 years and the building of equity over time. Let’s delve into these factors to gain a better understanding of the financial impact over the long-term.

Total Interest Paid Over 20 Years

When choosing a mortgage term, it’s essential to consider the total interest paid over the entire repayment period. With a 5-year term and 20-year amortization, the interest is calculated based on the 20-year timeline, but the mortgage term is only five years. This means that at the end of the five-year term, the mortgage will need to be refinanced or renewed.

During the 5-year term, regular mortgage payments will be made, consisting of both principal and interest. It’s important to note that the interest paid during this period is based on the interest rate at the time of the mortgage’s initiation. However, at the end of the five-year term, when the mortgage is renewed, a new interest rate may be applied.

To determine the total interest paid over 20 years, it is necessary to evaluate the interest portion of each mortgage payment made during the five-year terms. By summing up these interest payments over the four renewal periods and adding them to the interest paid during the initial five-year term, one can determine the total interest paid over the entire 20-year amortization period.

Building Equity With 20 Year Amortization

One of the advantages of opting for a 20-year amortization is the accelerated building of equity. Equity refers to the value of the homeowner’s stake in the property and increases over time as mortgage payments are made. With a shorter amortization period like 20 years, the homeowner builds equity faster compared to longer-term amortizations.

As each mortgage payment is made, a portion goes towards the principal, reducing the outstanding balance. Consequently, the homeowner’s equity in the property increases. Building equity is essential for various reasons, including opportunities for future borrowing, investments, or potential refinancing options.

It’s important to note that opting for a 20-year amortization may result in higher mortgage payments compared to longer-term options. However, the trade-off is the ability to quickly build equity and own the property outright in a shorter period.

Choosing The Right Mortgage Structure

One of the most important decisions you’ll make when it comes to your mortgage is choosing the right structure. Understanding the differences between the various terms and amortizations is crucial to finding a mortgage that best fits your financial goals. In this article, we’ll explore the concept of 5-year term and 20-year amortization and provide key considerations for making the right choice.

Considerations For Different Terms And Amortizations

When selecting a mortgage structure, it’s vital to analyze the terms and amortizations available to you. Let’s delve deeper into what a 5-year term and 20-year amortization entails:

A 5-year term refers to the length of time you commit to a specific interest rate and lender before renegotiating or renewing your mortgage. During this time, you’ll make regular payments to reduce your principal and interest. With a 20-year amortization, you spread out your mortgage payments over a longer period, which results in smaller monthly installments compared to a shorter amortization.

Here are some key considerations when deciding on the right term and amortization:

| Consideration | Explanation |

|---|---|

| Long-term Stability | A longer-term provides stability with a fixed interest rate, shielding you from potential rate fluctuations. This is especially beneficial if you’re looking for predictability and plan on staying in your home for a considerable period. |

| Flexibility | Shorter terms offer flexibility, allowing you to reassess your mortgage structure more frequently. This can be advantageous if you anticipate changes in your financial situation or plan to sell your property in the near future. |

| Monthly Payments | The shorter the amortization, the higher your monthly payments will be. A longer amortization can ease your financial burden by spreading out the payments, making it more manageable in the short term. However, keep in mind that a longer amortization may result in paying more interest over time. |

| Equity Building | Choosing a shorter amortization helps you build equity in your home at a faster pace. This can be significant if you plan to tap into your home’s equity for future purposes such as renovations or investments. |

Seeking Professional Advice

While considering different mortgage structures, it’s highly recommended to seek professional advice from a mortgage broker or financial advisor. They can help assess your financial situation, future plans, and guide you towards the most suitable term and amortization based on your specific needs and goals. Their expertise ensures you make an informed decision and avoid any potential pitfalls.

By understanding the implications of a 5-year term and 20-year amortization and considering the various factors outlined above, you can confidently choose a mortgage structure that aligns with your financial strategy and aspirations.

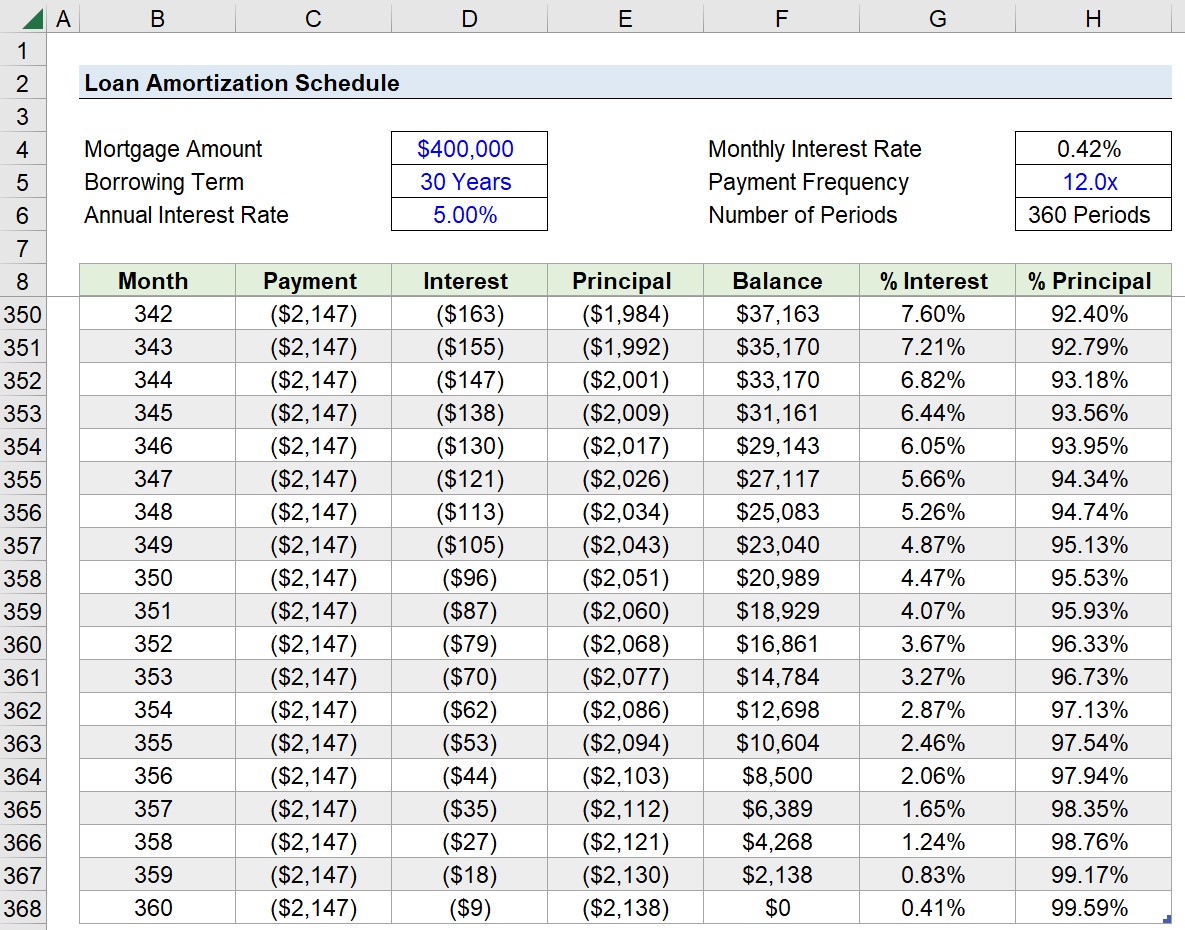

Credit: www.wallstreetprep.com

Frequently Asked Questions On What Does 5 Year Term 20 Year Amortization Mean?

What Is A 5-year Term With A 20-year Amortization?

A 5-year term with a 20-year amortization refers to a mortgage loan where the borrower pays off the loan over a 20-year period, but the interest rate and other terms are fixed for only the first 5 years. After the initial 5-year term, the interest rate may be adjusted, and the borrower may choose to refinance or continue with a new term.

How Does A 5-year Term With A 20-year Amortization Affect Monthly Payments?

With a 5-year term and a 20-year amortization, the monthly payments are typically lower compared to a shorter amortization period. However, it’s important to note that after the initial 5-year term, the interest rate may change, which can increase or decrease the monthly payments depending on the new rate.

Is A 5-year Term With A 20-year Amortization Suitable For Me?

The suitability of a 5-year term with a 20-year amortization depends on your financial goals and circumstances. If you plan to stay in your home for a short period and want lower monthly payments, it may be a good option.

However, if you plan to stay long-term or are concerned about potential rate increases after the initial term, you may want to consider other options.

Conclusion

Understanding the meaning of a 5-year term and a 20-year amortization is crucial for your financial planning. It determines your repayment schedule and overall cost. With this knowledge, you can make informed decisions and choose the right mortgage option for your needs.

Keep this in mind as you navigate your real estate endeavors.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is a 5-year term with a 20-year amortization?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “A 5-year term with a 20-year amortization refers to a mortgage loan where the borrower pays off the loan over a 20-year period, but the interest rate and other terms are fixed for only the first 5 years. After the initial 5-year term, the interest rate may be adjusted, and the borrower may choose to refinance or continue with a new term.” } } , { “@type”: “Question”, “name”: “How does a 5-year term with a 20-year amortization affect monthly payments?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “With a 5-year term and a 20-year amortization, the monthly payments are typically lower compared to a shorter amortization period. However, it’s important to note that after the initial 5-year term, the interest rate may change, which can increase or decrease the monthly payments depending on the new rate.” } } , { “@type”: “Question”, “name”: “Is a 5-year term with a 20-year amortization suitable for me?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The suitability of a 5-year term with a 20-year amortization depends on your financial goals and circumstances. If you plan to stay in your home for a short period and want lower monthly payments, it may be a good option. However, if you plan to stay long-term or are concerned about potential rate increases after the initial term, you may want to consider other options.” } } ] }