How Does an Amortization Schedule Work? : The Ultimate Guide

An amortization schedule outlines the repayment plan for a loan, including the principal amount and interest payments, demonstrating how the balance decreases over time with each payment. This schedule serves as a financial roadmap, informing borrowers about their loan balance and how much interest they will pay throughout the loan term.

It breaks down each payment into principal and interest portions, illustrating the decreasing interest and increasing principal contributions as the loan progresses. With this schedule, borrowers can track their progress, make informed financial decisions, and better understand the cost of borrowing.

Implementing an amortization schedule can assist in budgeting, planning for future payments, and determining how extra payments may impact the loan term.

The Basics Of Amortization Schedule

An amortization schedule outlines the repayment of a loan over time, breaking down each payment into the portion that goes towards interest and the portion that reduces the principal balance. It helps borrowers understand how much they owe and the total interest paid over the loan term.

What Is An Amortization Schedule?

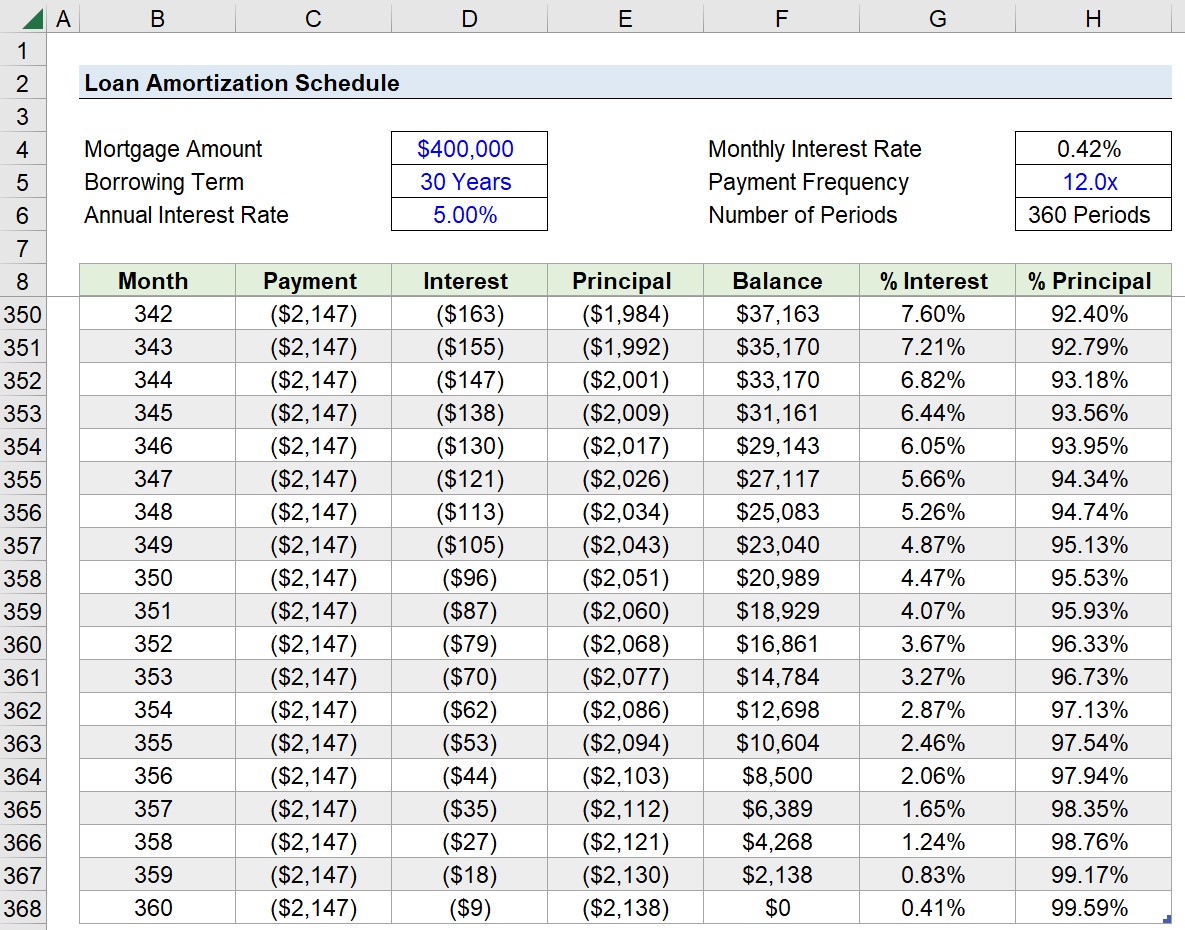

An amortization schedule is a useful tool that helps borrowers understand the payment structure of a loan. It provides a detailed breakdown of each payment, showing how much goes towards the principal balance and how much goes towards interest. This schedule is essential for planning and budgeting purposes, as it allows borrowers to see how their loan balance decreases over time.Components Of An Amortization Schedule

In order to fully grasp how an amortization schedule works, it’s important to understand its key components. These components include:- Loan amount: This is the total amount borrowed from the lender.

- Loan term: This refers to the length of time in which the loan must be repaid. It is typically measured in months or years.

- Interest rate: This is the percentage that the lender charges on the outstanding loan balance.

- Monthly payment: This is the fixed amount that the borrower needs to pay each month to repay the loan within the agreed-upon term.

- Principal balance: This is the remaining amount owed on the loan.

Credit: www.wallstreetprep.com

Importance Of Understanding Amortization Schedule

Understanding the amortization schedule is crucial in comprehending how it works. This schedule outlines the payment plan, interest, and principal amount, enabling borrowers to manage their finances effectively.

When it comes to financial planning and loan repayment, understanding the concept of an amortization schedule is crucial. This schedule outlines the repayment process of a loan, offering a clear visualization of how payments are applied to the principal and interest over time. By having a solid understanding of how an amortization schedule works, you can make informed decisions regarding your finances and ensure that you stay on track with your loan repayment.

Financial Planning

Understanding the ins and outs of an amortization schedule is an essential aspect of effective financial planning. This schedule provides valuable insights into the repayment process, allowing you to create a budget and allocate funds accordingly. By examining the schedule, you can identify the exact amount of principal and interest you will be paying each month, helping you plan for future expenses and avoid any potential financial strain. Additionally, the amortization schedule can assist you in estimating the overall cost of the loan, enabling you to evaluate its affordability and assess potential alternatives.

Loan Repayment Visualization

An amortization schedule offers a unique visual representation of the loan repayment process, making it easier to grasp the concept and track your progress. This visual aid showcases the distribution of monthly payments towards interest and principal, allowing you to observe how the balance reduces over time. With this visualization, you gain a clearer understanding of how each payment contributes to reducing your overall debt and can motivate yourself to stay on top of your repayment plan. This clarity and transparency empower you to make adjustments or accelerate payments if you wish to pay off the loan faster.

How To Read An Amortization Schedule

An amortization schedule is an essential tool for understanding the repayment structure of a loan. It provides a detailed breakdown of each payment’s allocation toward principal and interest, helping borrowers comprehend the financial implications of their loan. Here’s how to read an amortization schedule:

Understanding Payment Allocation

An amortization schedule consists of a series of payment periods, typically monthly, with each entry detailing the amount allotted to principal and interest for that specific month. The schedule also shows the remaining balance after each payment and the cumulative interest paid. It’s crucial to pay attention to how the payment allocation changes over time. In the initial stages, a higher proportion of the payment goes towards interest, while as time progresses, a greater portion is directed at paying down the principal.

Spotting Interest And Principal Payments

When examining an amortization schedule, it’s important to distinguish between the portions allotted to interest and principal. During the early stages of a loan, the interest component is typically higher, gradually decreasing as the principal is paid down. Identifying these components enables borrowers to comprehend how their payments are reducing the overall indebtedness over time.

Credit: www.quickenloans.com

The Impact Of Extra Payments On Amortization Schedule

When it comes to paying off a loan, understanding how an amortization schedule works is crucial. This schedule breaks down your monthly payments into equal installments that go towards both the principal and the interest. However, making extra payments can have a significant impact on this schedule – it can help to reduce interest costs and shorten the loan term. Let’s explore how these extra payments can make a difference.

Reducing Interest Costs

Extra payments on your loan can lead to a substantial reduction in interest costs over time. By paying more than the required monthly payment, you are essentially chipping away at the principal amount. This means you are decreasing the overall balance that accrues interest. So, the extra payments allow you to save on the interest charges that would otherwise accumulate over the life of the loan.

Here’s an example to illustrate the impact: Suppose you have a $100,000 loan with a 5% interest rate and a 30-year term. By paying an extra $100 every month, you’ll end up saving over thousands of dollars in interest and shorten the loan term. Plus, you’ll have the added benefit of clearing your debt sooner!

Shortening The Loan Term

In addition to reducing interest costs, making extra payments can also help you shorten the loan term. By consistently paying more than the required amount, you’ll be able to pay off the loan faster. The extra payments go towards the principal, accelerating the reduction of the outstanding balance, and ultimately decreasing the overall duration of the loan.

For example, let’s consider the same scenario as above, a $100,000 loan with a 5% interest rate and a 30-year term. By making an additional payment of $100 each month, you could potentially pay off the loan three to four years earlier than the original term. Imagine the relief of being debt-free sooner!

Conclusion

By understanding the impact of extra payments on an amortization schedule, you can make informed decisions about managing your loans. By reducing interest costs and shortening the loan term, extra payments not only save you money but also help you achieve financial freedom sooner. So, if you have the means, consider making those additional payments and enjoy the benefits of a faster or less expensive loan repayment!

Common Mistakes To Avoid With Amortization Schedules

Understanding how an amortization schedule works is crucial when it comes to managing your mortgage payments effectively. However, there are a few common mistakes that many people make when dealing with these schedules. By avoiding these errors, you can ensure that you have a clear picture of your loan repayment and make more informed financial decisions. In this post, we will discuss two common mistakes that borrowers often encounter in relation to amortization schedules:

Ignoring The Total Interest Paid

One of the major mistakes borrowers make with their amortization schedule is overlooking the total interest paid over the life of the loan. While it’s easy to focus solely on the monthly payment, disregarding the total interest can lead to surprises down the line. By understanding the total interest paid, you can better assess the long-term cost of your loan and make informed decisions about refinancing or paying off your mortgage early.

Avoiding this mistake requires taking a closer look at your amortization schedule. You will notice that initially, a significant portion of your monthly payment goes towards paying interest, with a smaller amount allocated toward the principal. However, over time, the balance shifts, and more of your payment goes toward paying down the principal. By keeping this in mind and regularly reviewing your amortization schedule, you can track the decrease in total interest paid and stay on top of your loan progress.

Failing To Account For Escrow Payments

An additional common mistake borrowers make is failing to account for escrow payments in their amortization schedules. Escrow payments typically include the property taxes and homeowners insurance, which are bundled with your mortgage payment and held in a separate account. These funds are then used to pay these expenses when they become due.

To avoid this mistake, it’s important to review your amortization schedule and determine if it includes escrow payments. If not, you will need to factor in the estimated amount for property taxes and homeowners insurance when calculating your total monthly housing cost. By including these expenses and regularly updating your amortization schedule, you can ensure that you are not caught off guard by sudden financial obligations.

Understanding the common mistakes associated with amortization schedules can save you from unnecessary surprises and ensure a smoother loan repayment process. By being aware of the total interest paid and accounting for escrow payments, you can make more informed decisions about your mortgage and manage your finances more effectively.

Credit: www.occupier.com

Frequently Asked Questions For How Does An Amortization Schedule Work?

How Does An Amortization Schedule Work?

An amortization schedule is a table that shows how a loan is gradually paid off over time. It breaks down each payment into its principal and interest components, allowing borrowers to see how much they still owe and how much interest they are paying.

Can I Change The Terms Of My Amortization Schedule?

Once an amortization schedule is set, the terms are usually fixed. However, some lenders may allow borrowers to make changes if certain conditions are met. It’s best to consult with your lender to see if modifications are possible.

What Are The Benefits Of An Amortization Schedule?

An amortization schedule allows borrowers to plan their finances and budget effectively. It shows how much of each payment goes towards principal and interest, helping borrowers understand the true cost of their loan and make informed decisions.

How Can An Amortization Schedule Help Me Save Money?

By analyzing your amortization schedule, you can identify opportunities to save money. Making extra payments towards the principal or refinancing the loan when interest rates are lower can help you pay off the loan sooner and reduce the overall interest paid.

Conclusion

Understanding how an amortization schedule works is crucial for managing debt and making informed financial decisions. By breaking down loan repayment into manageable installments, the schedule helps borrowers track their progress and plan for the future. With this knowledge, individuals can take control of their finances and achieve long-term stability.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “How does an amortization schedule work?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “An amortization schedule is a table that shows how a loan is gradually paid off over time. It breaks down each payment into its principal and interest components, allowing borrowers to see how much they still owe and how much interest they are paying.” } } , { “@type”: “Question”, “name”: “Can I change the terms of my amortization schedule?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Once an amortization schedule is set, the terms are usually fixed. However, some lenders may allow borrowers to make changes if certain conditions are met. It’s best to consult with your lender to see if modifications are possible.” } } , { “@type”: “Question”, “name”: “What are the benefits of an amortization schedule?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “An amortization schedule allows borrowers to plan their finances and budget effectively. It shows how much of each payment goes towards principal and interest, helping borrowers understand the true cost of their loan and make informed decisions.” } } , { “@type”: “Question”, “name”: “How can an amortization schedule help me save money?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “By analyzing your amortization schedule, you can identify opportunities to save money. Making extra payments towards the principal or refinancing the loan when interest rates are lower can help you pay off the loan sooner and reduce the overall interest paid.” } } ] }