How Does a Pik Loan Work? Boost Your Profits with a Pik Loan!

A Pik loan works by allowing the borrower to obtain additional debt secured by the collateral of an existing loan. We will explore how a Pik loan functions and the benefits and risks associated with this type of financing.

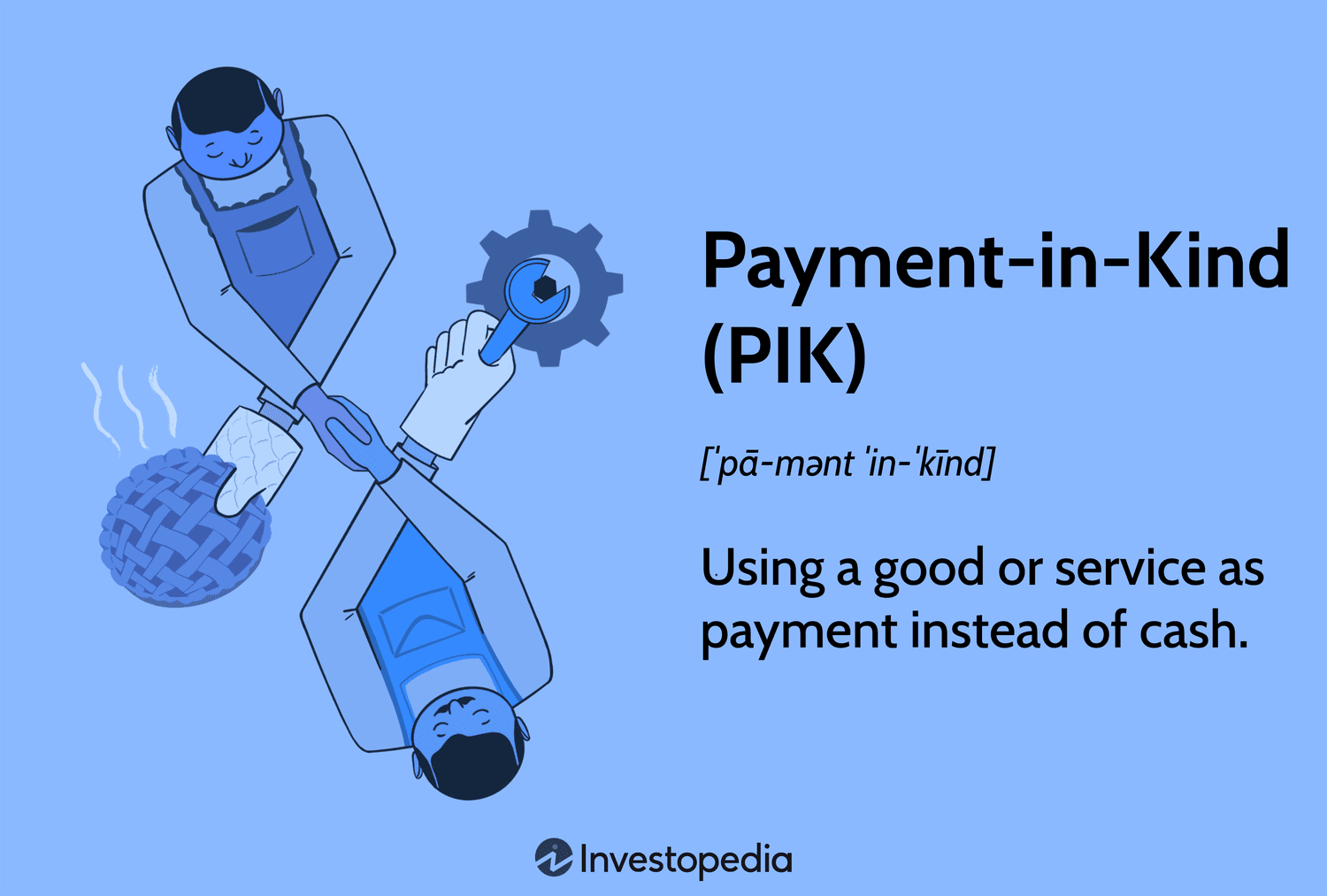

A Pik loan, also known as a payment-in-kind loan, is a form of debt that enables a borrower to obtain additional funding while deferring interest payments. Rather than making cash payments, the borrower has the option to pay the interest by issuing additional debt.

This type of loan is often used when the borrower faces financial constraints or when traditional financing options are limited. However, Pik loans typically come with higher interest rates and additional risks, making it important for borrowers to carefully evaluate their ability to service the debt. In the following sections, we will delve deeper into the mechanics, advantages, and drawbacks of Pik loans.

Credit: www.freepik.com

What Is A Pik Loan?

A Pik loan, also known as payment-in-kind loan, allows borrowers to pay interest through additional borrowed funds rather than cash. This type of loan enables potential borrowers with limited cash flow to pay off their interest using more debt, which can be beneficial in certain financial situations.

A Pik loan stands for Payment-in-Kind loan, which is a type of financing that allows borrowers to make interest payments in the form of additional borrowed funds rather than cash. Essentially, it enables the borrower to defer cash interest payments and instead accrue debt. This can be an attractive option for companies that require immediate funding but lack the necessary cash flow to make interest payments in the short term.

Advantages Of A Pik Loan

1. Flexibility: Pik loans provide borrowers with the flexibility to defer cash interest payments, offering some relief during challenging financial periods.

2. Preserves Cash Flow: By deferring interest payments, companies can conserve their cash flow and allocate funds towards other critical business needs, such as expansion or operational expenses.

Example: A growing business might need to invest in new equipment or hire additional staff to meet increasing customer demand. With a Pik loan, the company can divert its cash flow towards these areas instead of interest payments, supporting its growth strategy.

3. Improved Liquidity: Pik loans enhance a company’s liquidity position by providing access to additional borrowed funds that can be used for various purposes, including working capital requirements and debt refinancing.

4. Enhanced Financial Flexibility: With a Pik loan, companies have greater financial flexibility because they can choose when and how to repay the debt. This enables them to align repayments with their projected cash flow and financial milestones, minimizing the risk of default.

5. Potential Tax Benefits: In certain jurisdictions, the interest expense on Pik loans may be tax-deductible, offering a potential advantage for borrowers. However, it is essential to consult with a tax professional to understand the specific tax implications in your jurisdiction.

Risks Of A Pik Loan

1. Increased Debt Burden: By deferring cash interest payments, borrowers accrue additional debt over time, increasing their overall debt burden. This can have long-term implications for the company’s financial health and creditworthiness.

2. Higher Interest Costs: Pik loans typically carry higher interest rates compared to traditional loans. The added interest expense, compounded by the deferment of cash payments, can significantly increase the total cost of borrowing.

3. Risk of Default: The deferral of cash interest payments in a Pik loan exposes borrowers to the risk of default if they are unable to meet their repayment obligations when they become due. This can lead to severe financial consequences, including penalties, legal action, and damage to the company’s credit profile.

4. Limited Availability: Pik loans may not be easily accessible for all borrowers, as lenders often require detailed financial information and perform thorough due diligence to mitigate the risks associated with this type of financing.

5. Complex Structures: Pik loans can have complex structures with various terms and conditions that borrowers must thoroughly understand before entering into an agreement. It is crucial to engage with legal and financial advisors to ensure full comprehension of the loan terms and potential implications.

Credit: www.fastcapital360.com

How Does A Pik Loan Work?

How Does a Pik Loan Work?

A Pik loan, also known as a “Payment-in-Kind” loan, is a type of financing that allows borrowers to defer principal and interest payments for a certain period of time. This type of loan is commonly used in situations where the borrower is in need of short-term cash flow relief and is willing to make higher payments in the future. The unique characteristic of a Pik loan lies in its repayment structure, which differs from traditional loans. Let’s explore the key aspects of how a Pik loan works.

Pik Loan Structure

A Pik loan typically consists of two components: cash interest and PIK interest. Cash interest refers to the interest that is paid periodically in cash, similar to a regular loan. On the other hand, PIK interest stands for “Payment-in-Kind” interest and allows the borrower to accumulate interest and add it to the loan balance instead of paying it in cash.

Pik Loan Repayment Terms

The repayment terms of a Pik loan vary and can be tailored to the needs of the borrower and lender. Typically, the loan is structured in a way that allows the borrower to defer principal payments during the initial period, with only cash interest being paid. This provides the borrower with immediate cash flow relief. However, it’s important to note that eventually, the accumulated PIK interest must be repaid.

A commonly used structure for Pik loans is the “bullet maturity,” where the loan is due in full at a predetermined maturity date. At this point, the borrower must repay the entire loan balance, including the accumulated PIK interest. Alternatively, the loan might be structured with periodic principal payments over the term, gradually reducing the loan balance. This repayment option may be more manageable for borrowers who prefer a longer repayment period.

Strategies For Maximizing Pik Loan Benefits

Maximizing the benefits of a Pik loan requires a strategic approach that leverages its unique features. By understanding the various investment opportunities and implementing effective debt management strategies, borrowers can optimize the advantages of Pik loans.

Investment Opportunities

When utilizing Pik loans, it’s essential to identify lucrative investment opportunities that can generate high returns. Real estate ventures, small business expansions, and venture capital investments are potential avenues for allocating funds acquired through Pik loans. These options present the opportunity for substantial growth and profitability, making them attractive choices for maximizing the benefits of a Pik loan.

Debt Management

Managing debt effectively plays a pivotal role in maximizing the benefits of a Pik loan. By strategically allocating the loan proceeds towards consolidating high-interest debt and paying off existing liabilities, borrowers can improve their financial position and reduce overall interest expenses. Additionally, implementing cash flow management, such as optimizing revenue streams and reducing unnecessary expenses, can further enhance the effectiveness of the Pik loan in achieving financial objectives.

Regulatory Considerations

A Pik loan operates under specific regulatory considerations that determine its functioning. This type of loan involves priority interest payments to certain stakeholders, providing flexibility and options to borrowers within legal boundaries. Understanding these regulatory factors is crucial to comprehending how a Pik loan works.

The regulatory landscape plays a crucial role in any lending arrangement, and a Pik loan is no exception. As with any financial instrument, there are compliance requirements that lenders and borrowers must adhere to, as well as potential impacts on financial reporting. Let’s explore these key considerations in detail.Compliance Requirements

Complying with regulatory requirements is of utmost importance when it comes to obtaining and maintaining a Pik loan. Lenders must ensure that they meet all legal and regulatory obligations, including anti-money laundering (AML) laws, know-your-customer (KYC) rules, and state and federal lending regulations. These compliance requirements help protect against fraudulent activities and ensure transparency in the lending process. It is crucial for lenders to have robust systems and processes in place to meet these compliance standards. For borrowers, compliance requirements may include providing detailed financial information, such as audited financial statements, income tax returns, and other relevant documents. Additionally, borrowers may need to demonstrate their ability to service the loan by meeting certain financial ratios or creditworthiness criteria. Understanding and fulfilling these compliance requirements is essential for both lenders and borrowers to navigate the complexities of a Pik loan successfully.Potential Impact On Financial Reporting

Obtaining a Pik loan can have implications for financial reporting, both for the lender and the borrower. The unique nature of a Pik loan may require careful consideration and analysis of the appropriate accounting treatment. Lenders must determine how to classify and disclose these loans on their financial statements, considering factors such as the likelihood of repayment and the terms of the loan. Properly categorizing Pik loans is crucial to provide accurate and transparent financial information to stakeholders. For borrowers, the accounting treatment of a Pik loan can impact their financial statements as well. The loan proceeds may need to be recognized as a liability, and interest expense will need to be recorded over the loan term. Understanding the accounting treatment of a Pik loan is essential for borrowers to ensure compliance with accounting standards, accurately present their financial position, and meet reporting obligations. In conclusion, regulatory considerations are a critical aspect of understanding how a Pik loan works. Compliance requirements and the potential impact on financial reporting must be carefully navigated by both lenders and borrowers. By staying abreast of regulatory obligations and accounting standards, stakeholders can effectively manage the complexities associated with Pik loans.Conclusion And Recommendations

A pik loan allows borrowers to defer interest payments, increasing overall debt. To maximize its potential, it’s important to carefully consider repayment plans and consult with a financial advisor to make informed decisions.

Evaluating The Suitability Of Pik Loans

In evaluating whether a Pik loan is suitable for your specific financial needs, it is important to consider several factors. Firstly, your ability to meet the increased debt service requirements should be carefully assessed. If you are confident in your ability to generate sufficient cash flow and repay the additional interest, a Pik loan could be a viable option.

Secondly, it is essential to analyze the risks associated with this type of financing. Understanding the potential consequences of defaulting on the Pik loan and the impact it can have on your overall financial stability is crucial.

Furthermore, you should assess the current and future market conditions in your industry. Determining whether the market is strong enough to support the increased debt burden and sustain your business operations is vital. Obtaining market research reports and consulting with industry experts can equip you with valuable insights.

Staying Informed About Market Trends

Once you have obtained a Pik loan, it is crucial to stay informed about market trends that may affect your business’s financial health. Regularly monitoring economic indicators, industry reports, and competitive analysis will enable you to make informed decisions and adapt your strategy accordingly.

Additionally, establishing relationships with key stakeholders in your industry such as suppliers, customers, and competitors can provide you with valuable market intelligence. Networking events, conferences, and trade shows are great opportunities to connect with relevant industry players.

Moreover, utilizing technology tools such as analytics software and financial management systems can help you track and analyze important data. Generating timely reports and conducting periodic reviews of your financial performance will enable you to identify potential risks and opportunities.

In conclusion, evaluating the suitability of a Pik loan should involve a comprehensive assessment of your financial capacity, understanding of risks involved, and analysis of market conditions. Staying informed about market trends allows you to adapt your strategies and make informed decisions to ensure the successful repayment of the loan.

:max_bytes(150000):strip_icc()/Mezzanine_Financing_Final-6293dcdc9ade49c2a546d328a1732030.png)

Credit: www.investopedia.com

Frequently Asked Questions For How Does A Pik Loan Work?

How Does A Pik Loan Work?

A Pik loan, also known as a payment-in-kind loan, allows borrowers to pay interest with additional borrowed funds instead of using cash payments. This type of loan is usually used by companies with inadequate cash flow to cover debt payments.

Instead of making regular cash interest payments, borrowers have the option to pay the interest with more borrowed funds. However, it’s important to note that Pik loans are considered high-risk and can be expensive due to the added interest charges.

What Are The Advantages Of A Pik Loan?

One advantage of a Pik loan is that it provides flexibility in paying interest when cash flow is low, allowing borrowers to use their available funds for other business needs. Additionally, Pik loans can be helpful for companies with seasonal sales patterns or cyclical businesses since they can defer part of their interest payments during slower periods.

However, it’s essential to carefully consider the risks and costs associated with Pik loans before using them.

Are There Any Risks Associated With Pik Loans?

Yes, there are risks associated with Pik loans. Since the interest is paid with additional borrowed funds, the overall debt can increase rapidly, leading to a higher interest burden. This can potentially result in financial distress and limit the borrower’s ability to repay the loan.

Moreover, Pik loans often have higher interest rates and fees compared to traditional loans, making them more expensive in the long run.

How Do I Qualify For A Pik Loan?

Qualifying for a Pik loan typically requires demonstrating sufficient assets and collateral to secure the loan. Lenders will also assess the borrower’s cash flow, credit history, and ability to meet the loan terms. Moreover, the borrower’s financial stability and the industry’s overall performance can also influence the lender’s decision.

It’s recommended to consult with a financial advisor or loan specialist to understand the specific requirements and process for obtaining a Pik loan.

Conclusion

A Pik loan can be a valuable tool for investors seeking flexible financing options for real estate projects. By understanding the principles behind how a Pik loan works, investors can make informed decisions to maximize their investment potential. With its unique features, a Pik loan offers customization and convenience, making it a versatile choice for financing real estate ventures.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “How does a Pik loan work?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “A Pik loan, also known as a payment-in-kind loan, allows borrowers to pay interest with additional borrowed funds instead of using cash payments. This type of loan is usually used by companies with inadequate cash flow to cover debt payments. Instead of making regular cash interest payments, borrowers have the option to pay the interest with more borrowed funds. However, it’s important to note that Pik loans are considered high-risk and can be expensive due to the added interest charges.” } } , { “@type”: “Question”, “name”: “What are the advantages of a Pik loan?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “One advantage of a Pik loan is that it provides flexibility in paying interest when cash flow is low, allowing borrowers to use their available funds for other business needs. Additionally, Pik loans can be helpful for companies with seasonal sales patterns or cyclical businesses since they can defer part of their interest payments during slower periods. However, it’s essential to carefully consider the risks and costs associated with Pik loans before using them.” } } , { “@type”: “Question”, “name”: “Are there any risks associated with Pik loans?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, there are risks associated with Pik loans. Since the interest is paid with additional borrowed funds, the overall debt can increase rapidly, leading to a higher interest burden. This can potentially result in financial distress and limit the borrower’s ability to repay the loan. Moreover, Pik loans often have higher interest rates and fees compared to traditional loans, making them more expensive in the long run.” } } , { “@type”: “Question”, “name”: “How do I qualify for a Pik loan?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Qualifying for a Pik loan typically requires demonstrating sufficient assets and collateral to secure the loan. Lenders will also assess the borrower’s cash flow, credit history, and ability to meet the loan terms. Moreover, the borrower’s financial stability and the industry’s overall performance can also influence the lender’s decision. It’s recommended to consult with a financial advisor or loan specialist to understand the specific requirements and process for obtaining a Pik loan.” } } ] }