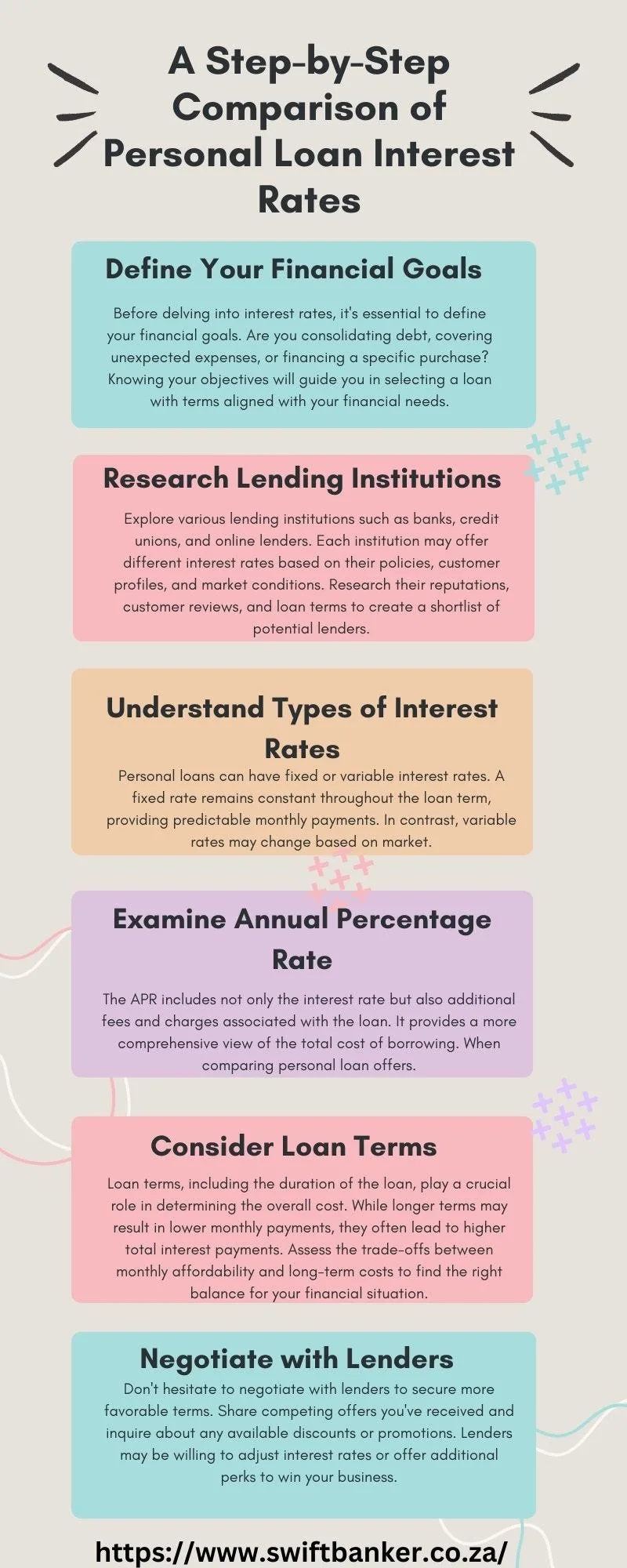

How Do You Explain Credit? Simplify Your Understanding with These Essential Tips.

Credit is a financial concept that involves borrowing money, usually from a bank or financial institution, with the promise to repay it in the future. It is an arrangement where the borrower receives access to funds that they can use for various purposes, such as buying goods or services, and they agree to repay the borrowed amount along with any accrued interest over a specified period of time.

Credit is an essential part of the modern financial system. It allows individuals and businesses to access funds that they may not have readily available, enabling them to make purchases and investments. Understanding how credit works is crucial for managing personal finances and making smart financial decisions.

We will explain what credit is, how it works, and why it matters in today’s economy. Whether you’re considering applying for a loan or credit card, or simply want to broaden your financial knowledge, this guide will provide you with a clear understanding of the concept of credit.

Importance Of Credit

Credit plays a crucial role in our financial lives. It provides us with the ability to purchase goods and services, borrow money for major expenses, and build a solid foundation for our future. Understanding the importance of credit is essential for achieving financial stability. In this section, we will explore the impact credit has on our financial options and its role in our everyday lives.

Impact On Financial Options

Credit has a profound impact on our financial options. It determines our ability to obtain loans, secure favorable interest rates, and qualify for mortgages. By maintaining a good credit score, individuals gain access to better financial opportunities and can enjoy lower interest rates on credit cards and loans. This not only saves money in the long run but also enables us to reach our financial goals faster.

Role In Everyday Life

Credit plays a significant role in our everyday lives. It allows us to make important purchases such as buying a car or a home. Without credit, many of us would not be able to afford these big-ticket items. Additionally, credit is essential for establishing trust with lenders and financial institutions. Whether we are applying for a rental property or seeking a business loan, creditworthiness matters. A good credit history serves as a testament to our ability to manage debt responsibly, enhancing our chances of approval.

Components Of Credit

Understanding credit is essential for anyone looking to manage their finances effectively. When it comes to explaining credit, it’s important to break it down into its different components. This article will focus on two key components of credit: the credit score and the credit report.

Credit Score

A credit score is a three-digit number that represents an individual’s creditworthiness. It is a numerical reflection of a person’s financial history and borrowing behavior. Lenders use credit scores to assess the likelihood of a borrower repaying their debts on time. A higher credit score usually indicates responsible financial management, while a lower score may suggest a higher risk for lenders.

Factors that impact a credit score include:

- Payment history, including late payments or defaults

- Amount of outstanding debt

- Length of credit history

- Credit utilization ratio, which measures the amount of available credit being utilized

- Types of credit being used, such as credit cards or loans

It is important to maintain a good credit score as it can affect an individual’s ability to secure loans, get favorable interest rates, or even rent a home.

Credit Report

A credit report is a detailed record of an individual’s credit history. It includes information such as the person’s personal information, credit accounts, payment history, outstanding balances, and any negative information like late payments or bankruptcies. Lenders, landlords, and other financial institutions use credit reports to assess the risk associated with lending money or extending credit.

Key information found in a credit report includes:

| Personal Information | Credit Accounts | Payment History |

|---|---|---|

| Name, address, social security number | Credit cards, loans, mortgages | Record of on-time and late payments |

| Date of birth, employment history | Credit limits, balances, and available credit | Information on collections, defaults, or bankruptcies |

Monitoring your credit report regularly is crucial to ensure there are no errors or fraudulent activities that could impact your creditworthiness.

In conclusion, credit can be better understood by examining its components, such as the credit score and credit report. A good credit score is vital for financial opportunities, while the credit report provides a detailed history of an individual’s financial standing. Being aware of these components empowers individuals to make informed financial decisions and work towards improving their creditworthiness.

Building Good Credit

Building good credit is crucial for financial stability and accessing favorable interest rates for loans and credit cards. It’s a reflection of your responsible financial behavior and can open doors to various opportunities. Here are some key strategies for establishing and maintaining good credit:

Managing Debt Responsibly

Debt management is essential for cultivating a healthy credit profile. Keep your credit utilization low, aiming for around 30% of your available credit. Avoid maxing out your credit cards as it can negatively impact your credit score.

Making Timely Payments

Punctual payment of bills and debts is vital for good credit. Missing due dates can result in late fees and negative marks on your credit report. Setting up automatic payments or reminders can help you stay on top of your finances and demonstrate diligence to lenders.

:max_bytes(150000):strip_icc()/FinancialLiteracy_Final_4196456-74c34377122d43748ed63ef46a285116.jpg)

Credit: www.investopedia.com

Consequences Of Poor Credit

Credit refers to the trustworthiness of an individual’s financial obligations. Poor credit can result in higher interest rates, difficulty securing loans, and limited financial opportunities. It is essential to maintain good credit to avoid the negative consequences that can hinder financial stability.

Understanding credit is essential for financial responsibility. When individuals have poor credit, it can lead to a range of consequences that affect their financial opportunities and stability. Here, we discuss two major consequences of poor credit: limited financial opportunities and higher interest rates.

Limited Financial Opportunities

Poor credit can significantly restrict an individual’s access to financial opportunities. Lenders and financial institutions are hesitant to extend credit or loans to individuals with a history of poor credit. This limited access can make it difficult for those with poor credit to secure loans for major purchases, such as a home or car. Additionally, individuals may struggle to qualify for credit cards or favorable interest rates on loans.

Furthermore, individuals with poor credit may find it challenging to rent an apartment or obtain certain types of insurance. Landlords and insurance companies often rely on credit history when evaluating potential tenants or clients. Without a strong credit history, individuals with poor credit may face additional barriers in securing housing or obtaining insurance coverage.

Higher Interest Rates

Poor credit can result in higher interest rates on loans and credit cards. Lenders consider individuals with poor credit to be higher-risk borrowers, and consequently, they charge higher interest rates to compensate for that risk. This means that individuals with poor credit may face significantly higher interest costs on loans, making it more challenging to repay their debts.

Higher interest rates can have a long-term impact on an individual’s financial health. When interest rates are high, it becomes increasingly difficult to pay off debts, which can lead to a cycle of accumulating more debt. This cycle can further damage an individual’s credit score, making it even harder to improve their financial situation.

Overall, poor credit has far-reaching consequences, including limited financial opportunities and higher interest rates. It is essential for individuals to be aware of these potential repercussions and take proactive steps to improve their credit health.

Improving Credit Score

Your credit score plays a critical role in your financial life. A good credit score opens doors to better loan terms, lower interest rates, and the ability to qualify for various financial opportunities. If you’re wondering how to improve your credit score, there are a few strategies you can employ. In this section, we will discuss how to identify errors in your credit report and reduce credit card balances, both of which can have a significant impact on improving your credit score.

Identifying Errors In Credit Report

Errors in your credit report can negatively affect your credit score. It’s essential to regularly review your credit report and identify any discrepancies that may be dragging down your score. Here’s how you can do it:

- Obtain a free copy of your credit report from one of the major credit bureaus, such as Experian, TransUnion, or Equifax.

- Thoroughly examine each section of the report, including personal information, credit accounts, and payment history.

- If you spot any errors or inaccuracies, such as accounts you never opened or incorrect payment information, gather supporting documentation.

- File a dispute with the credit bureau(s) to have the errors investigated and corrected. You can typically initiate the dispute process online through the credit bureau’s website.

By actively monitoring your credit report for errors and promptly addressing them, you can improve the accuracy of your credit information, which may lead to a higher credit score.

Reducing Credit Card Balances

Your credit card balances play a significant role in determining your credit score. High credit card balances can indicate a higher risk for lenders, potentially leading to a lower credit score. Here are some effective ways to reduce your credit card balances:

- Create a budget to track your monthly income and expenses. Identify areas where you can cut back on spending to free up money to pay down your credit card balances.

- Prioritize your credit card debts by focusing on paying off the card with the highest interest rate first, while making minimum payments on the other cards.

- Consider transferring high-interest balances to a card with a lower interest rate or utilizing a personal loan to consolidate your debts.

- Avoid making new charges on your credit cards while you work on reducing your balances. This will prevent your debt from spiraling out of control.

- Set up automatic payments or reminders to ensure you make your credit card payments on time each month, avoiding late fees and potential negative impacts on your credit score.

By diligently reducing your credit card balances and staying on top of your payments, you can gradually improve your credit score.

Credit: www.linkedin.com

Credit: www.scribbr.com

Frequently Asked Questions On How Do You Explain Credit?

What Is Credit Explained Simply?

Credit is a simple concept where you borrow money or use a credit card to purchase goods or services. It’s like a loan that you must pay back with interest over time. It can help you make big purchases, but remember to manage it responsibly to avoid debt.

What Is Credit In Your Own Words?

Credit is the ability to borrow money or receive goods and services with the understanding that you will pay for them later. It allows you to make purchases and fulfill your needs even if you don’t have immediate cash.

How Would You Describe Your Credit?

My credit is a reflection of my financial history and track record of paying bills. It shows my trustworthiness to lenders for getting loans or credit cards.

What Is Credit In Short Note?

Credit is a financial term that refers to the ability to borrow money or the amount of money that is owed. It is a measure of trustworthiness for a borrower, indicating their ability to repay debts.

Conclusion

Understanding credit is crucial for financial success. By comprehending its impact on borrowing and purchasing power, individuals can make informed decisions. It’s essential to maintain a good credit score to access favorable financial opportunities. Remember, responsible credit management is the key to securing a stable and secure financial future.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is credit explained simply?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Credit is a simple concept where you borrow money or use a credit card to purchase goods or services. It’s like a loan that you must pay back with interest over time. It can help you make big purchases, but remember to manage it responsibly to avoid debt.” } } , { “@type”: “Question”, “name”: “What is credit in your own words?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Credit is the ability to borrow money or receive goods and services with the understanding that you will pay for them later. It allows you to make purchases and fulfill your needs even if you don’t have immediate cash.” } } , { “@type”: “Question”, “name”: “How would you describe your credit?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “My credit is a reflection of my financial history and track record of paying bills. It shows my trustworthiness to lenders for getting loans or credit cards.” } } , { “@type”: “Question”, “name”: “What is credit in short note?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Credit is a financial term that refers to the ability to borrow money or the amount of money that is owed. It is a measure of trustworthiness for a borrower, indicating their ability to repay debts.” } } ] }