What is a Type 2 Student Loan? : All You Need to Know

A Type 2 student loan is a specific type of loan available to students. It requires financial need for eligibility and offers lower interest rates than other types of student loans.

Pursuing higher education often comes with significant financial burdens, which many students rely on loans to alleviate. One such loan option is the Type 2 student loan. This particular loan type is designed for students who can demonstrate financial need, offering them an opportunity to access funds at lower interest rates compared to other student loan options.

Whether it covers tuition fees or helps with living expenses, a Type 2 student loan aims to provide students with the necessary financial support to pursue their educational goals. Understanding the details and requirements of this loan is crucial for students seeking affordable ways to finance their education.

Credit: www.ramseysolutions.com

Understanding Type 2 Student Loans

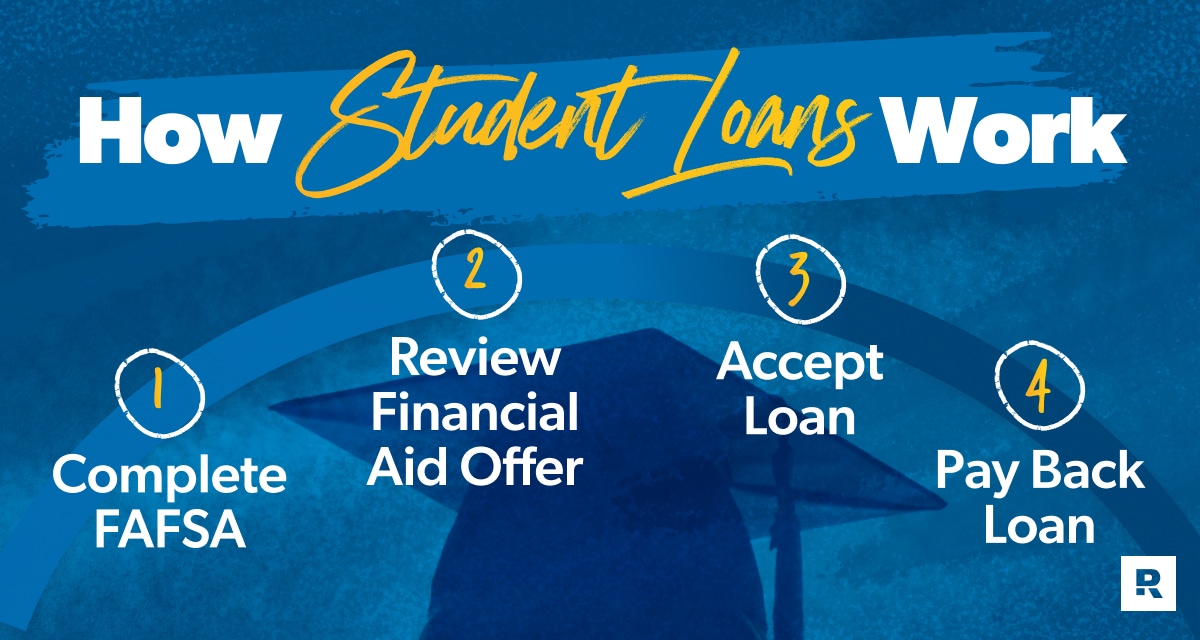

In the world of higher education, student loans are a common way for students to finance their studies. One type of student loan that you may come across is the Type 2 student loan. Understanding what a Type 2 student loan means and who qualifies for it is crucial for students seeking financial assistance for their education. In this post, we will explore everything you need to know about Type 2 student loans, from what they are to the qualification criteria you need to meet.

What Are Type 2 Student Loans?

Type 2 student loans, also known as subsidized loans, are a form of financial aid offered to students based on their financial need. Unlike other types of student loans, Type 2 loans do not accumulate interest while the student is in school or during deferment periods. This means that the government pays the interest on the loan while the student is still enrolled in school. This feature can help alleviate the financial burden on students and make repayment more manageable after graduation.

Qualification Criteria

To be eligible for a Type 2 student loan, there are certain criteria that you must meet. These criteria generally include:

- Demonstrating financial need: Type 2 student loans are need-based loans, which means that your financial situation will be evaluated to determine if you qualify.

- Enrollment in an eligible institution: You must be enrolled at least part-time in an eligible college, university, or vocational school to be eligible for a Type 2 loan.

- Being a U.S. citizen or eligible non-citizen: Type 2 loans are typically available to U.S. citizens, permanent residents, and certain eligible non-citizens.

- Maintaining satisfactory academic progress: You must meet the academic standards set by your institution to remain eligible for Type 2 student loans.

Meeting these qualification criteria is essential to be considered for a Type 2 student loan. It is important to note that the specific requirements and eligibility may vary depending on the lender and loan program.

In conclusion, Type 2 student loans are a beneficial form of financial assistance for students with demonstrated financial need. Understanding the basics of Type 2 loans, including what they are and the qualification criteria, can help students make informed decisions about their education and financing options.

Repayment Options

If you’ve taken out a Type 2 student loan, it’s important to understand the repayment options available to you. These options determine how you’ll pay back the money you borrowed for your education. With careful consideration of your financial situation, you can select the most suitable repayment plan that aligns with your needs. Let’s explore two common types of repayment plans for Type 2 student loans: the Standard Repayment Plan and Income-Driven Repayment Plans.

Standard Repayment Plan

The Standard Repayment Plan is the conventional method for repaying a Type 2 student loan. With this plan, your loan is divided into equal monthly payments over a fixed period, usually 10 years. This repayment option allows you to pay off your loan in a reasonable timeframe while keeping your monthly payments consistent. The fixed monthly payments include both principal and interest, along with any additional fees. By sticking to the Standard Repayment Plan, you can ensure steady progress towards full loan repayment.

Income-driven Repayment Plans

If your financial circumstances make it challenging to make the fixed monthly payments of the Standard Repayment Plan, an Income-Driven Repayment (IDR) Plan may be a suitable solution. These plans adjust your monthly payments based on your income and family size. There are several IDR plans available, such as the Income-Based Repayment (IBR) Plan, the Pay As You Earn (PAYE) Plan, and the Revised Pay As You Earn (REPAYE) Plan. These plans typically require borrowers to pay a portion of their discretionary income towards their student loans. Monthly payments can be as low as 10% of your discretionary income, making it more manageable for those with lower incomes.

One advantage of Income-Driven Repayment Plans is the potential for loan forgiveness after a certain period. Depending on the plan and your circumstances, your remaining loan balance could be forgiven after 20 or 25 years of consistent repayment. However, it’s important to note that forgiven amounts may be subject to income taxes in the year they are discharged.

While the Income-Driven Repayment Plans offer more flexibility, it’s crucial to understand that these options may result in a longer repayment term and potentially higher total interest paid over the life of the loan. Evaluating your financial situation and considering the pros and cons of each plan will help you determine which repayment option is best for you.

Interest Rates And Subsidization

Interest rates and subsidization play a crucial role in the world of type 2 student loans. Understanding the nuances of fixed vs. variable interest rates and subsidized vs. unsubsidized loans is essential for making informed decisions about your education financing.

Fixed Vs. Variable Interest Rates

When it comes to type 2 student loans, borrowers may encounter the choice between fixed and variable interest rates. A fixed interest rate remains constant throughout the life of the loan, providing predictability and stability. In contrast, a variable interest rate fluctuates based on the current market conditions, potentially resulting in lower initial rates but also posing the risk of future increases.

Subsidized Vs. Unsubsidized Loans

Another fundamental consideration in the realm of type 2 student loans pertains to subsidized and unsubsidized loans. Subsidized loans are awarded based on financial need, and the government covers the interest while the borrower is in school at least half-time, during the grace period, and during deferment. On the other hand, unsubsidized loans are available to all eligible students regardless of financial need, but the borrower is responsible for the interest from the time the loan is disbursed.

Credit: studentaid.gov

Benefits And Drawbacks

A Type 2 student loan offers flexible repayment options and lower interest rates. However, it requires a credit check and may have higher eligibility criteria compared to other student loans. Borrowers can benefit from manageable repayment plans, but may face stricter qualification requirements.

Benefits and Drawbacks Type 2 student loans offer several advantages and drawbacks that students should consider before making a decision. Understanding these benefits and drawbacks will help you assess if a Type 2 loan is the right choice for your educational needs. In this article, we will explore both the benefits and potential disadvantages of Type 2 student loans.Advantages Of Type 2 Loans

Type 2 student loans come with a range of advantages that make them an attractive option for many students. Here are some key benefits worth considering:- Flexibility: Type 2 loans offer flexible repayment terms and options, allowing you to tailor the repayment plan based on your financial circumstances.

- Lower interest rates: Compared to private loans, Type 2 loans generally come with lower interest rates, helping you save money over the course of repayment.

- Deferment and forbearance options: Type 2 loans often provide deferment or forbearance options, allowing you to temporarily pause or reduce your loan payments in case of financial hardships or unexpected circumstances.

- Loan forgiveness programs: Depending on your career path, you may qualify for loan forgiveness programs, such as public service loan forgiveness, which can help eliminate a portion of your Type 2 loan debt.

- Income-driven repayment plans: Type 2 loans offer income-driven repayment plans, which adjust your monthly payments based on your income, making them more manageable.

Potential Disadvantages

While Type 2 student loans offer significant benefits, it’s important to be aware of potential drawbacks. Here are some disadvantages to consider:- Accruing interest: Type 2 loans accrue interest while you’re in school and during any deferment or forbearance periods, which means your loan balance may increase over time if you’re not making regular payments.

- Longer repayment period: Type 2 loans typically have longer repayment periods compared to private loans. This can result in more interest paid over the life of the loan.

- Limited eligibility: Eligibility for Type 2 loans may be limited and dependent on various factors, such as financial need or enrollment in an accredited educational institution.

- Non-dischargeable in bankruptcy: Unlike some other types of debt, Type 2 student loans are generally not dischargeable in bankruptcy, which means you’ll be responsible for repaying them even in the event of financial hardship.

- Potential impact on credit score: Failing to make consistent loan payments can negatively impact your credit score, making it harder to secure future loans or credit.

Loan Forgiveness And Discharge

When it comes to student loans, the idea of loan forgiveness and discharge can be a saving grace for many borrowers. Understanding the eligibility for forgiveness and the circumstances for discharge is vital for those burdened by the weight of a Type 2 student loan. If you’re wondering if you qualify for loan forgiveness or if there are circumstances that could lead to discharge, read on to find out!

Eligibility For Forgiveness

If you’re hopeful for loan forgiveness, the good news is that there are specific criteria you must meet to be eligible. While each forgiveness program may have different requirements, here are some common eligibility factors:

- Working in a public service job: If you work full-time for a government or nonprofit organization, you may qualify for the Public Service Loan Forgiveness (PSLF) program. This program encourages individuals to pursue careers in public service and offers forgiveness after making 120 qualifying payments.

- Teaching in a low-income school: Teachers who work in low-income schools or educational service agencies may be eligible for the Teacher Loan Forgiveness program. Depending on factors like years of service and the subject you teach, you could have a portion of your loan forgiven.

- Income-driven repayment plans: Enrolling in an income-driven repayment plan, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), can also lead to loan forgiveness. After making payments for a certain period of time (usually 20-25 years), the remaining balance may be forgiven.

Circumstances For Discharge

In certain situations, your Type 2 student loan can be discharged, meaning you are no longer responsible for repaying the loan. Some common circumstances that can lead to discharge include:

- Permanent disability: If you experience a permanent and total disability that prevents you from working and repaying your loan, you may qualify for a Total and Permanent Disability (TPD) discharge. This discharge can provide financial relief in challenging times.

- School closure: If your school closes while you’re enrolled or shortly after you withdraw, you may be eligible for a Closed School Discharge. This discharge erases your debt and helps alleviate the burden of a loan tied to an education that was disrupted.

- Fraud or false certification: In cases where your school engaged in fraudulent activities or falsely certified your eligibility, you may qualify for a discharge. This means you are not responsible for repaying the loan, freeing you from the consequences of deceptive practices.

Understanding the options for loan forgiveness and discharge is crucial for those seeking relief from the financial strain of a Type 2 student loan. By meeting the eligibility criteria or experiencing qualifying circumstances, you can find a light at the end of the loan repayment tunnel.

Credit: studentaid.gov

Frequently Asked Questions On What Is A Type 2 Student Loan?

What Is A Type 2 Student Loan?

A Type 2 student loan is a federal loan that offers fixed interest rates and allows students to borrow money for educational expenses. Unlike Type 1 loans, Type 2 loans require students to start repaying the loan while still in school.

How Do I Qualify For A Type 2 Student Loan?

To qualify for a Type 2 student loan, you must be enrolled at least half-time in an eligible educational institution. You also need to complete the Free Application for Federal Student Aid (FAFSA) and meet the eligibility criteria, including demonstrating financial need.

Can I Defer My Type 2 Student Loan Payments?

Yes, you can defer your Type 2 student loan payments while you are enrolled in school at least half-time. However, interest will continue to accrue during the deferment period, so it’s important to weigh your options and consider making interest payments to avoid increased loan costs.

Conclusion

A Type 2 student loan is a valuable resource for students needing financial assistance. Understanding the eligibility criteria, interest rates, and repayment options is essential for making informed decisions. By staying informed and proactive, students can effectively manage their financial obligations and focus on their education.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is a Type 2 Student Loan?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “A Type 2 student loan is a federal loan that offers fixed interest rates and allows students to borrow money for educational expenses. Unlike Type 1 loans, Type 2 loans require students to start repaying the loan while still in school.” } } , { “@type”: “Question”, “name”: “How do I qualify for a Type 2 student loan?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “To qualify for a Type 2 student loan, you must be enrolled at least half-time in an eligible educational institution. You also need to complete the Free Application for Federal Student Aid (FAFSA) and meet the eligibility criteria, including demonstrating financial need.” } } , { “@type”: “Question”, “name”: “Can I defer my Type 2 student loan payments?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes, you can defer your Type 2 student loan payments while you are enrolled in school at least half-time. However, interest will continue to accrue during the deferment period, so it’s important to weigh your options and consider making interest payments to avoid increased loan costs.” } } ] }